By Jeanette Rice, Americas Head of Investment Research, CBRE

Despite still strong fundamentals in hotel operating performance, the capital markets environment for the hotel sector has been going through choppy waters this year. A brief review of key investment metrics illustrates some of the challenges.

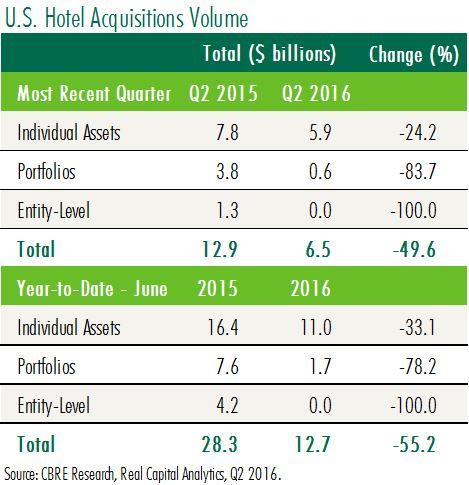

Hotel Investment Remains Subdued Tepid hotel investment activity continued in Q2 2016. U.S. hotel acquisitions totaled $6.5 billion in Q2 2016, down 50% year-over-year. Similarly, the H1 2016 total reflects a 55% decline from H1 2015.

Fortunately, the year-over-year drop in single-asset purchases was less severe. Buying activity of individual assets provides a better measure of investment momentum, and H1 2016’s $11 billion total reflected a more moderate drop of -33% compared to last year.

Subdued buying activity in H1 2016 was partly the result of the turmoil in the CMBS market since CMBS capital traditionally has served as a much more important source of financing for hotels than for other property sectors. Investor sentiment has also certainly been influenced by less robust economic growth this year and greater concern about the near-term outlook (even though occupancy rates, ADRs and RevPARs are favorable this year).

Other factors for the H1 2016 subdued investment volume included a) limited portfolio purchases, b) no acquisitions of hotel companies, and c) no mega hotel acquisitions. However, Q3 2016 is more promising for the investment totals, if for no other reason that Marriott International’s $12 billion acquisition of Starwood Hotels & Resorts was approved by shareholders in April 2016 and will likely close in Q3 2016.

Acquisitions by cross-border buyers totaled $1.9 billion or a quite high 29.5% of the $6.5 billion total by all investor groups during the quarter. The Q2 cross-border investment total also represented a 10.6% rise over the prior year. China, Germany and Canada were the largest country sources of global capital.

H1 2016 investment volumes exceeded $500 million in seven U.S. metros. New York City remained the undisputed leader for attracting hotel investment capital followed by Washington, D.C., Chicago, Los Angeles, Miami/South Florida, Boston and Seattle.

Hotel Cap Rates Widen U.S. hotel cap rates averaged 7.84% for stabilized CBD assets and 8.39% for suburban assets according to CBRE’s North American Cap Rate Survey H1 2016 (to be published later this month). Both averages reflected modest widening. Cap rates for luxury assets in the CBD as well as suburbs experienced the smallest increases, while the largest increases were observed in suburban full-service and select-service hotels (+19 and 22 bps, respectively).

The largest increases in cap rates were also observed in Tier II markets (secondary markets), particularly in the non-luxury categories of hotels.

NCREIF Return Improves Modestly from Q1 2016 NCREIF returns, the best industry measure of performance of owned hotel assets, provide a mixed picture for the sector. The Q2 2016 return for institutionally-owned hotels of 1.5% (-0.8% appreciation, 2.3% income) reflected slightly improved performance compared to Q1 2016 (total return of 1.2%). However, it remained well below 2015’s average quarter return of 3.2%.

For the year ending Q2 2016, the hotel sector experienced a 9.5% return (appreciation 1.4%, income 8.0%), which represented a substantial downward shift from 2015’s 11.1%, mostly due to lower appreciation (not income). However, the Q2 2016 annual return remained substantially above the 15-year average of 6.8%.

Debt Metrics Send Mixed Message On the debt side of capital markets, measures of activity and performance also display mixed results. With respect to hotel lending activity, the Mortgage Bankers Association’s Quarterly Index of Commercial Mortgage Originations shows that hotel mortgage lending maintained an active level in Q2 2016 when compared to the prior quarter (+26%), but slipped 11% year-over-year.

CMBS issuance for hotel assets totaled $4.4 billion in H1 2016, down 70% from H1 2015 according to Commercial Mortgage Alert. Among all sectors, hotels has been the hardest hit by contraction in CMBS lending, but all sectors experienced year-over-year declines.

For life insurance companies, hotel mortgage production totaled a very moderate $791 million in Q1 2016 according to the American Council of Life Insurers or 5.4% of all life company lending in the quarter. The Q1 2016 total also represented a 29% decline year-over-year. (No 2Q data are available yet.) Hotel mortgage production totals by banks, the other major source of financing, are not available.

CMBS delinquency rates provide one picture of the performance of hotel mortgages. In CMBS portfolios, the hotel delinquency rate in June was 3.0%. The rate reflected a year-over-year decline of 18 bps. However, the recent monthly data suggest that hotel delinquency rates have stabilized.

While the maturing 2006-2007 vintage loans in CMBS pools provide some cause for concern in the industry, this concern mostly involves office and retail loans, which have the largest market shares in CMBS and currently are underperforming other sectors.

Nevertheless, because hotels are more dependent on CMBS capital than other sectors, as hotel loans mature, the health of the CMBS market will play a significant role in the success of refinancing the loans.

Additionally, over H1 2016, hotels have experienced the highest loss severity rates among the major property types (63% according to Morningstar, vs. the average for all property types of 47%), so refinancing may become a larger issue in the marketplace.

Outlook The second half of 2016 may not look dramatically different than the first half. Well, certainly, as noted above, the Starwood Hotels & Resorts acquisition will certain boost the investment totals. Moreover, if a few more portfolio sales materialize these could change the investment volume bottom line.

Financing hotel acquisitions will remain problematic given the CMBS market and the unlikelihood of a rapid turnaround here. But banks may step into the arena and play a greater role in financing hotel acquisitions. Cap rates which have been edging up for a year now may continue to see modest further widening over the balance of 2016.

Hotel investment strategy is more closely tied to the economy than the other sectors because hotel performance is impacted more quickly by changes in the economic performance. Sustained nervousness about the economy could keep potential investment dollars from transacting, even with very favorable property fundamentals. Yet, if the U.S. economy strengthens in the second half of the year (as is currently expected), if the outlook for 2017 improves, and if the risk of recession diminishes, then hotel investor sentiment is very likely to experience comparable improvement. And even if this does not all happen, the hotel sector may see improved investment activity from a few contrarians who recognize the opportunity to buy well performing assets at less than peak pricing.