By Robert Mandelbaum

For the past several years, limited- and select-service hotels have been extremely popular among hotel developers. According to STR, Inc. 80 percent of the properties (70 percent of the rooms) that opened in 2015 did not offer a restaurant. Also lagging in development activity are independent hotels. Of the 775 new hotels that opened in 2015, only 79 (10.2%) were not affiliated with a brand. These trends are the result of consumer preferences and the realities of financially feasible hotel development.

So, what happens if you are a hotelier with a passion for food and beverage and independence? You open a boutique hotel with an emphasis on restaurant and lounge service.

Back in the 1980s, development of boutique hotels was all the rage. Pioneers like Bill Kimpton, Chip Conley, and Ian Schrager founded their respective hotel chains that were quickly and enthusiastically accepted by travelers. In general, these hotels provided unique guest experiences that embraced and promoted high quality food and beverage outlets. The popularity of these hotels spawned boutique concepts such as W and Indigo that were affiliated with major international hotel brands. Over time, the growth of the Kimpton and Joie De Vive (Commune) portfolios has led to the perception of these chains as brands.

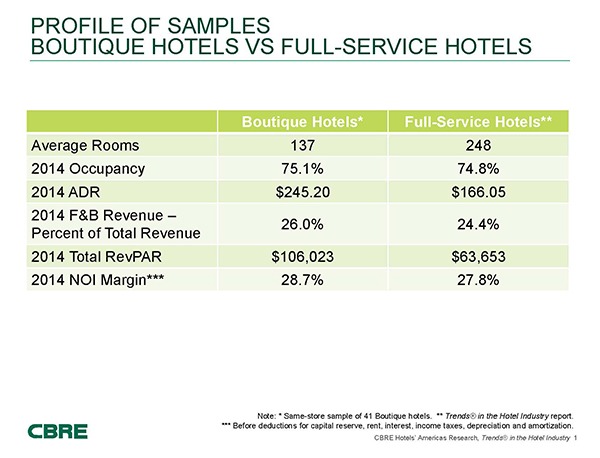

Per STR, Inc. there are 371 independent boutique hotels in the U.S. that operate a restaurant. To analyze the performance of today’s independent, full-service boutique hotels, we examined the performance of 41 independent, full-service boutique hotels for which we have annual operating statements each year from 2010 through 2014. In 2014 (latest annual data available) these 41 properties averaged 137 rooms in size, and achieved an occupancy level of 75.1 percent and an average daily rate of $245.20.

The performance of these independent boutique hotels was compared to the operating results of the full-service hotels sample in our annual Trends® in the Hotel Industry reports for the past five years. The following paragraphs summarize the results of our analysis.

Performance During Recovery

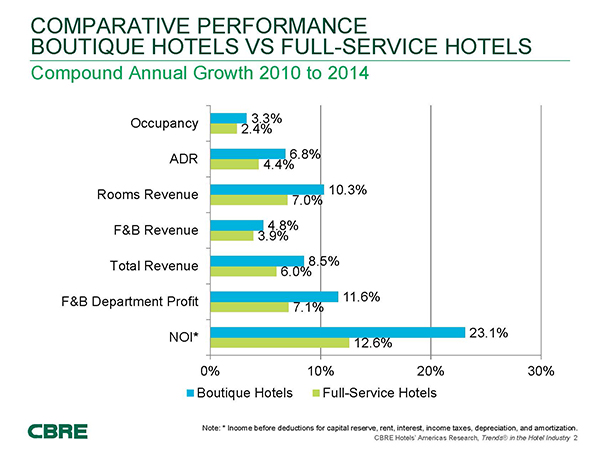

During the period 2010 through 2014, independent, full-service boutique hotels delivered greater growth on both the bottom and top lines compared to the sample of all full-service properties. Revenue per Available Rooms (RevPAR) for the boutique sample increased at a compound annual growth rate (CAGR) of 10.3 percent during this five year stretch compared to an increase of 7.0 percent for the all full-service sample. Boutique hotels achieved annual growth rate premiums in both occupancy and ADR.

Further, the independent, boutique hotels achieved greater growth in food and beverage revenue, which led to loftier increases in total revenue. The superior revenue growth resulted in a more rapid pace of profit recovery. From 2010 through 2014, the net operating income (NOI) of the independent, boutique hotels increased at a CAGR of 23.1 percent compared to a 12.6 percent NOI growth rate for all full-service properties.

F&B Department Comparison

As expected, food and beverage service takes on a greater role at independent, boutique properties compared to their traditional full-service hotel counterparts. From 2010 through 2014, food and beverage revenue at the boutique properties averaged 27.8 percent compared to 25.3 percent for the full-service sample. Consistent with overall lodging industry trends, this ratio to total revenue has declined for both samples since 2010. This is indicative of the relatively strong growth in the demand and pricing for renting hotel rooms compared to the lag in recovery observed for other guest expenditures.

The difference in the composition of food and beverage revenue between the two samples is indicative of the relative market positioning of independent, boutique properties versus traditional full-service hotels. In 2014, revenue earned from restaurants and bars represented 52.5 percent of total food and beverage revenue at boutique hotels compared to just 36.9 percent at the full-service hotels. Owners and operators of independent, boutique properties are able to express their creativity by placing a greater emphasis on the development and marketing their restaurant and lounge concepts.

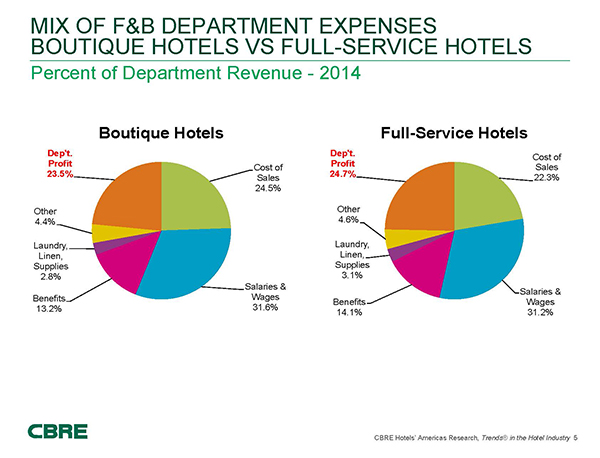

Conversely, the full-service properties earn a greater percentage of their food and beverage revenue from banquet business. This can be attributed to the larger size of the full-service properties (248 rooms) versus the boutique hotels (137 rooms), and subsequent orientation towards group demand. At traditional full-service hotels revenue from banquet food and beverage, meeting room rental, audio/visual, and service charges equaled 58.8 percent of total department revenue during 2014. This compared to 42.7 percent at the boutique hotels.

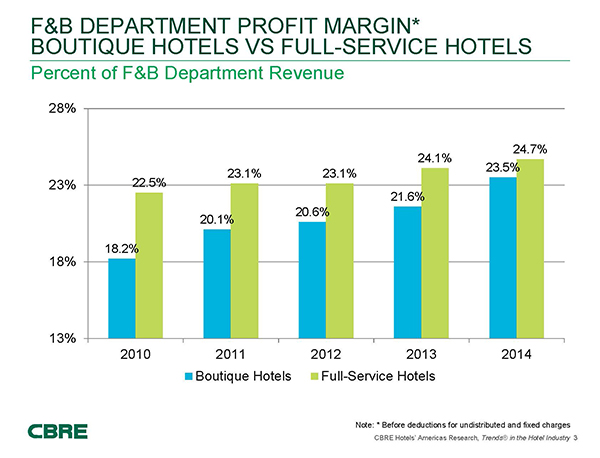

Given the higher percentage of banquet related revenue, full-service properties achieve greater efficiencies in the food and beverage department. In 2014, the traditional full-service hotels earned a food and beverage department profit margin of 24.7 percent versus 23.5 percent for the boutique properties.

Passion Required

The emergence of several new “lifestyle” brands shows the creativity that exists within the lodging industry. However, most of the creativity has been directed toward branded chains that offer limited amounts of food and beverage service. If you are a creative hotelier with an affection for food and beverage and desire to operate outside the mandates of an international chain, the opportunity exists to invest in an independent boutique hotel. However, before entering this segment of the industry, people must have a clear understanding of the financing, development, and operational challenges that exist.