By Robert Mandelbaum

Historically, if a guest notified the hotel 6 PM on the day of arrival that they would not be checking in, that was usually sufficient to waive any cancellation fees. However, given the proliferation of on-line booking programs that have empowered consumer’s purchasing practices, travelers have learned to take advantage of the fairly unrestrictive cancellation policies by booking multiple reservations and simply waiting until 5:59 PM to select the best rate. In turn, hotels were getting inflated reads on potential occupancy levels, which has a significant impact on revenue management decisions.

In an attempt to gain better control over their inventory and pricing, hotels have begun to tighten up their transient cancellation policies. Starting in 2015, some of the major hotel companies began to extend the time required by guests to provide notice that they will not be arriving and avoid being charged any cancellation fees. Prior to that, hotel companies introduced discounted non-refundable room rates similar to the airlines.

Per the Uniform System of Accounts for the Lodging Industry (USALI), the income received from transient reservation cancellations is recorded as Rooms Revenue and frequently difficult to identify as a discrete source of income on the standard hotel operating statement format. On the other hand, the fees hotels receive from the cancellation of group meetings are usually presented as a separate line item in Miscellaneous Income.

Because of the greater transparency, our firm is able to capture Cancellation and Attrition fee data when conducting our annual Trends® in the Hotel Industry survey. The USALI defines Cancellation Fees as “income received from transient guests and groups that cancel their reservations for guestrooms, food and beverage, and other services after a contracted or cutoff date.” Attrition fees are defined as “income received from groups that do not fulfill their guaranteed number of reservations for guestrooms, food and beverage, and other services.”

Based on a sample of 304 U.S. full-service, resort, and convention hotels that reported Attrition and Cancellation Fees each year from 2007 through 2014, we are able to analyze recent trends in this source of income.

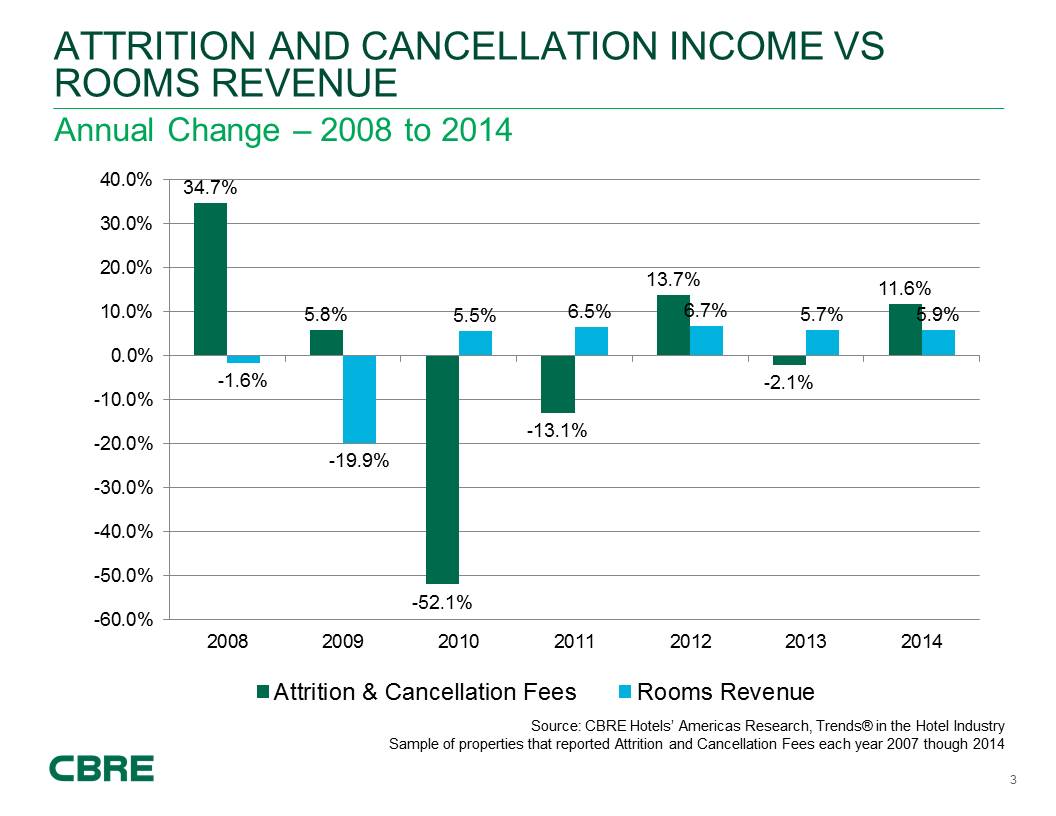

Changes in Fee Income When observing annual changes in Attrition and Cancellation Fee income from 2007 through 2014 we see correlations with the health of the overall U.S. lodging industry and the group demand segment.

In 2008, the initial year of the industry recession, the income from Attrition and Cancellation Fees increased by 34.7 percent over 2007. This was the result of the increased incidence of outright meeting cancellations, as well as shortfalls in meeting attendance. Attrition and Cancellation Income increased another 5.8 percent as the recession continued into 2009.

After 2009, this revenue source abruptly experienced two years of declines in 2010 (-52.1%) and 2011 (-13.1%). The declines can be attributed to a combination of fewer meetings, as well as some leniency in the inclusion of Attrition and Cancellation clauses contained in the group contracts that were negotiated during the depths of the recession in 2008 and 2009.

According to STR, accommodated group room nights in the U.S. returned to pre-recession levels in November of 2014. With the return of group demand, and high occupancy levels, hotel sales managers now feel empowered to be more aggressive in the inclusion and enforcement of Attrition and Cancellation policies.

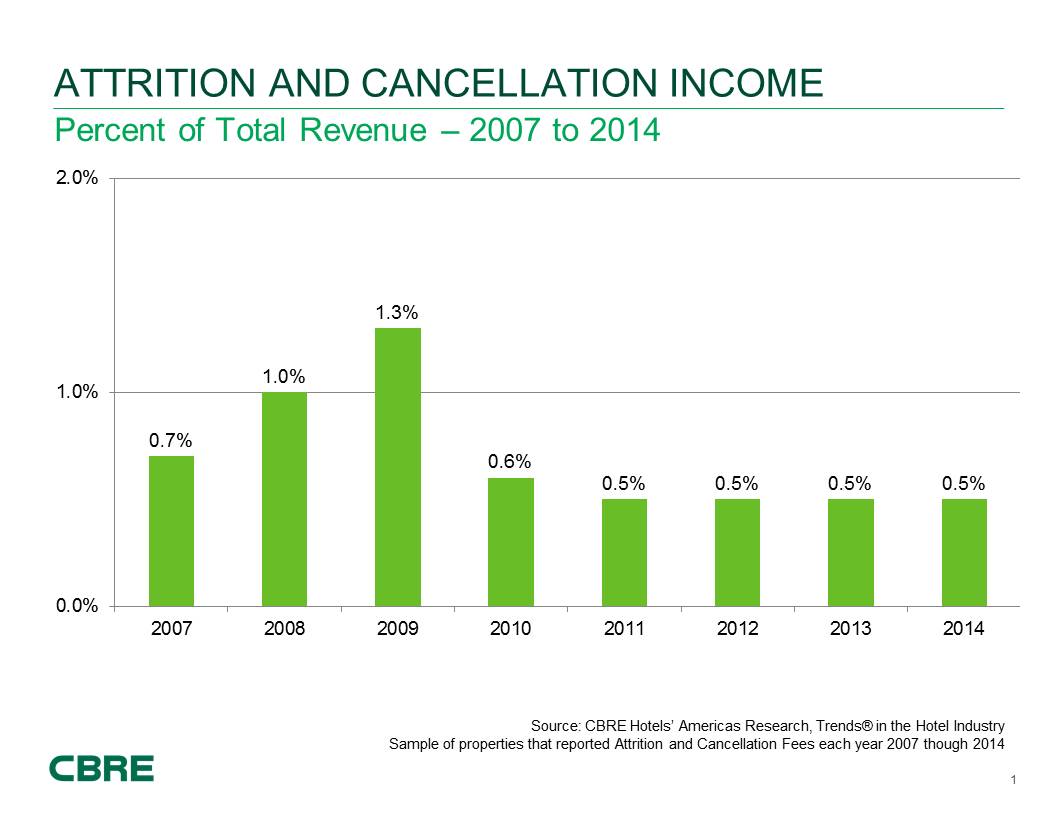

Contribution to Revenues

Given the previous mentioned changes in Attrition and Cancellation Fee income, this revenue source has fluctuated as a percentage of Total Revenue. In 2007, Attrition and Cancellation Income equaled 0.7 percent of Total Revenue. This metric jumped up to 1.3 percent in 2009, but has since leveled off at 0.5 percent of Total Revenue.

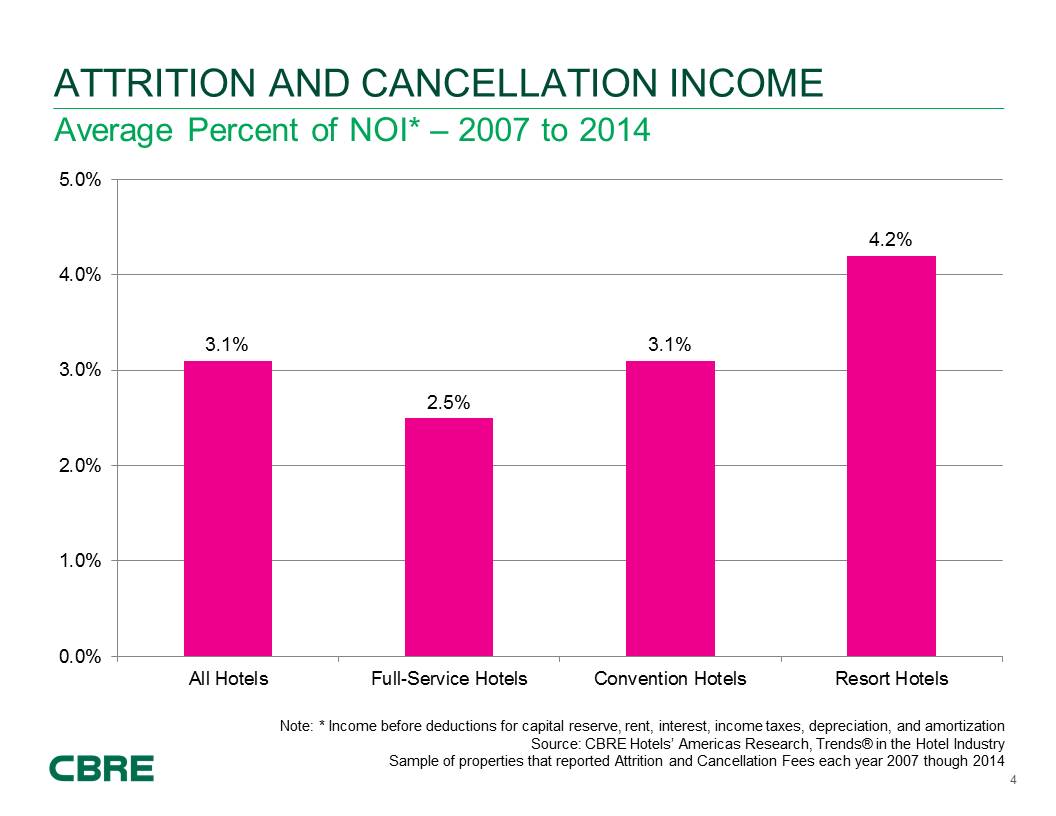

By property type, Attrition and Cancellation Revenue has been most significant as a source of revenue at resort hotels. From 2007 through 2014, this source of income averaged 0.9 percent of Total Revenue at resort hotels, followed by 0.8 percent at convention hotels and 0.5 percent at full-service properties. During the great recession, several corporate and association meetings scheduled to held at high-end resorts were cancelled to avoid the appearance of wasteful spending. This phenomenon became known as the AIG Effect.

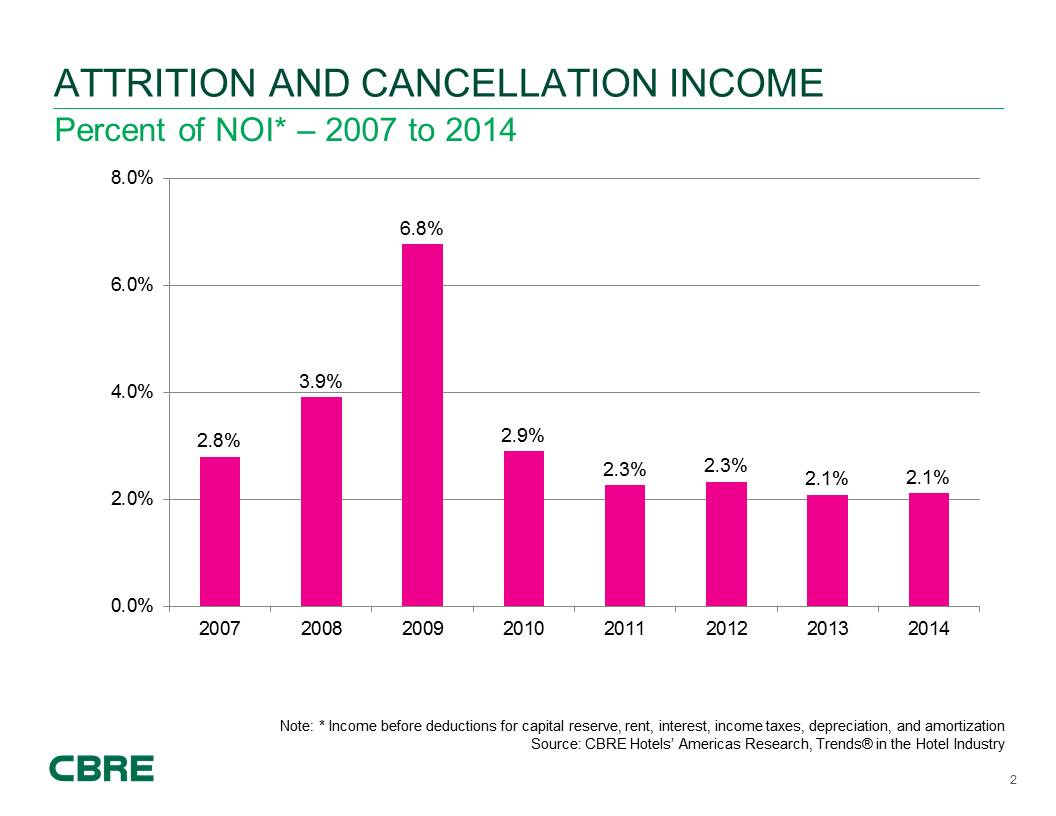

Contribution to Profits While Attrition and Cancellation Income has been a minor source of revenue for hotels, it can have a significant impact on profitability. Since a minimal amount of variable expense is incurred to earn Attrition and Cancellation revenue, it can be assumed that most of the penalty payments received by hotels drop right to the bottom-line. Accordingly, it is proper to analyze this source of revenue as a percent of net operating income (NOI).

As a percentage of NOI, Attrition and Cancellation Fees have averaged 3.1 percent from 2007 through 2014. In 2009, this ratio peaked at 6.8 percent. Once again, resort hotels have benefited the most among property types from Attrition and Cancellation Fees with an average NOI ratio of 4.2 percent.

Adapting Due mainly to recent advancements in guest-booking technology, hotels have only recently started to adjust their no-show policies regarding the cancellation of transient guest stays. However, changes in group Attrition and Cancellation policies have occurred frequently over the years as managers have adapted to current market conditions.

This article was published in the May 2016 edition of Lodging.