advertisement

One

Night Stands Are Expensive

|

News for the Hospitality Executive |

advertisement

One

Night Stands Are Expensive

|

By:

Robert Mandelbaum,

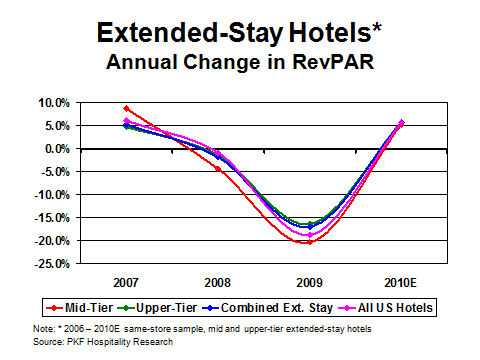

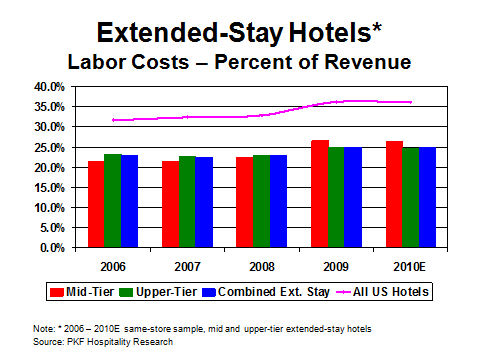

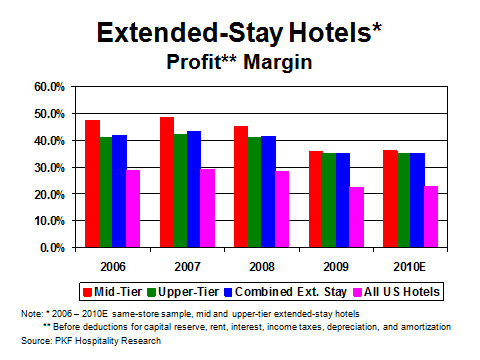

July 20, 2011 On paper, the formula for success at an extended-stay hotel is very sound. By accommodating guests for an extended period of time, these properties are able to “cover up” the soft spots on their calendars and achieve extraordinary annual levels of occupancy. In addition, the combination of limited services and amenities leads to increased employee productivity and high profit margins. As PKF Hospitality Research (PKF-HR) has noted in previous analyses, niche lodging products will achieve their intended market penetration and operating premiums during periods of economic prosperity, but are susceptible to derailment during times of stress. Extended-stay hotels are extremely dependent on multiple night stays to achieve their market positioning and operating efficiencies. What happens to these properties during an economic recession when relocations, multi-week trainings sessions, and large installation projects all get cut from corporate budgets? From its Trends® in the Hotel Industry database, PKF-HR analyzed the operating statements of 437 extended-stay hotels during the period 2006 through 2010 (estimated), the deepest industry recession on record. The research sample consisted of two groups; upper-tier (e.g. Residence Inn, Homewood Suites) and middle-tier (e.g. TownePlace Suites, Candlewood Suites). Lower-tier extended-stay properties (e.g. Homestead Studio Suites, Extended-Stay America) were excluded for confidentiality reasons. Comparisons were made to the aggregate performance of all property types in our Trends® survey. The Top Line All property types suffered declines in performance during the recent recession, including extended-stay hotels. However, on a relative basis, our sample of extended-stay properties achieved slightly less of a decline in RevPAR compared to the aggregate performance of all hotels in the Trends® survey. From 2007 to 2009, RevPAR for the extended-stay properties fell a cumulative 18.5 percent. This is less than the 19.5 percent decline experienced by the all hotel sample during the same period.  Expenses While greater levels of transient demand may have a positive impact on revenue, it does have a negative impact on the operating efficiencies of extended-stay hotels. With fewer check-ins and check-outs, extended-stay properties are usually able to reduce their housekeeping and front desk staffs. Accordingly, labors costs measured as a percent of total revenue typically run 10 to 12 percentage points less at extended-stay properties compared to industry wide averages. Despite a greater percentage decline in occupied rooms, extended-stay operators were not able to cut their labor costs as much as their counterparts at other property types. On average, salaries, wages, and employee benefits were reduced 10.0 percent for the entire Trends® sample from 2007 to 2009, but only 8.1 percent at the extended-stay properties. Managers at the properties in our extended-stay sample were able to cut their overall operating expenses by 7.1 percent from 2007 to 2009, but this pales in comparison to the 12.0 percent cost reductions achieved on average by all hotel operators.  Primarily attributable to the lower labor cost ratios, as well as the lack of retail food and beverage outlets and public space, extended-stay hotels achieve profit margins far superior to the 26.3 percent average for all hotels in the Trends® sample. During the four year study period, extended-stay hotels averaged a profit1 margin of 39.4 percent. The middle-tier extended-stay properties, with relatively fewer amenities and services, achieved a remarkable 42.6 percent average profit margin, while the upper-tier facilities brought a very respectable 38.9 percent of their revenues to the bottom line. Fortunately for extended-stay hotel managers, the relative ability to maintain RevPAR appears to have offset the inability to cut costs. From 2007 to 2009, net operating income1 declined 33.7 percent on average for the properties in the extended-stay sample. This is less than the 37.9 percent drop in profits for overall Trends® sample.  [1] Income before deductions for capital reserves, rent, interest, income taxes, depreciation, and amortization.  Robert

Mandelbaum is the Director of Research Information Services for PKF

Hospitality

Research. He is located in the firm’s

Atlanta office. For more information on

the Trends® in the Hotel Industry report,

please visit www.pkfc.com/store.

This article was published in the June 2011 edition of Lodging.

|

| Contact:

Robert Mandelbaum |

| Also See: | Hotel

Food and Beverage: Locals Up, Lounges Down / Robert Mandelbaum /

June 2011 |

| FREEBIES:

Hotels Give Some Things for Nothing / Robert Mandelbaum / April 2011 |

|

| Hang

Up The Phone And Hold The Starch, But Please Park The Car / Robert

Mandelbaum /February 2011 |

|

| Meeting

Planners Optimism Rising / Robert Mandelbaum / January 2011 |

|

| How

Profitable Will Your RevPAR Be In 2011? / Robert Mandelbaum /

December 2010 |

|

| No

Show – No Problem; Hotels Profit from Attrition and Cancellation Income

/ Robert Mandelbaum / November 2010 |

|

| Right

Direction - Wrong Amount: Hotel Managers Underestimated 2009 Declines

in Performance / Robert Mandelbaum / October 2010 |

|

| Surprised, or Stubborn? U.S. Hotel Managers Missed Their Budgets In 2008 / Robert Mandelbaum / October 2009 |