![]()

advertisement

LE's Asia Pacific Hotel Construction Pipeline Summary

China�s Economic Growth Makes

it a Top Priority for Global Hotel Companies

and Their Higher-end Brands

for Both New Construction and Reflagging

|

News for the Hospitality Executive |

![]()

advertisement

LE's Asia Pacific Hotel Construction Pipeline Summary

China�s Economic Growth Makes

it a Top Priority for Global Hotel Companies

and Their Higher-end Brands

for Both New Construction and Reflagging

|

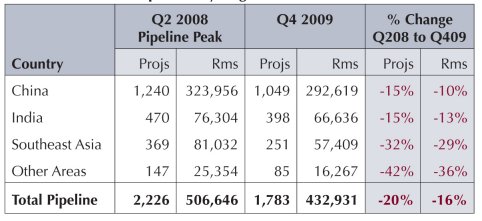

March 16, 2010 - At the end of Q4 2009, the Asia Pacific Pipeline stands at 1,783 projects/ 432,931 rooms. As a whole, Asia Pacific has one of the lowest percentage Pipeline decreases of any region from the peak in Q2 2008, second only to Africa. Because China has the second largest Pipeline in the world, total project counts for the region are off just 20% from the peak and total rooms by 16%. LE�s Construction Pipeline: By Region

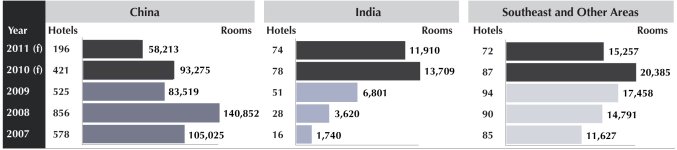

China and India, two of the fast growing and most resilient economies in the world, are acknowledged to be the world�s leading growth markets. Global companies have significant new construction and reflagging programs in these countries, particularly with their higher-end brands in China and with upscale and midscale brands in India. Pipelines for other countries in the rest of the region have been more susceptible to economic and lending pressures as experienced elsewhere in the world. Notable exceptions include Thailand, Vietnam, Indonesia and Malaysia, where economic declines have been less severe and the recoveries quicker to occur. China At 1,049 projects/292,619 rooms, China continues to represent the lion�s share of the Asia Pacific Pipeline, with 59% of all projects and 68% of rooms. China�s sustained economic growth makes it a top priority for global hotel companies and their higher-end brands for both new construction and reflagging opportunities. The increasing spending power and mobility of the country�s inhabitants are also a boon for the native Chinese economy brands who are expanding development programs in the suburbs of major business centers and smaller cities experiencing explosive population growth. The Chinese government continues to promote real estate development as a national priority. Throughout the last year, it directed its banking institutions to step up support for their development growth objectives. Recently, it has also been easier in China to raise equity capital through both public offerings and private investment sources than in other countries. Consequently, there are now concerns arising that a real estate bubble may be forming. To combat this, the government recently increased the amount of reserves lending institutions have to hold on deposit with central banks. As this new policy takes hold, financing for future projects is likely to become more difficult to obtain. Project migration up the Pipeline toward construction is down somewhat in Q4, but still moving at a moderate pace. A preponderance of construction starts in Q4 is native Chinese economy branded projects. Overall, New Project Announcements (NPAs) are in decline. But, there is an unusual occurrence that artificially boosted NPAs in Q4. 13 of China�s NPAs, with a total of 9,064 rooms, are projects that were previously put on hold by developers during an earlier, more restrictive lending period. With funding much easier to access today, they are now re-entering the Pipeline. They include 6 projects/6,455 rooms reactivated on the Cotai Strip, which also reflects the explosive growth of gaming in Macau. After the Olympics-driven peak in 2008, New Openings relaxed in 2009 with a total of 553 hotels/83,519 rooms coming online. 2010 is forecast to bounce back slightly with 421hotels/93,275 room scheduled to open that year, representing 72% of the region�s total New Hotel Openings that year. In 2011, New Openings will fall to the lowest level seen in years as 196 hotels/58,213 rooms are projected to enter new supply. India With 22% of Asia�s total projects and 15% of total rooms, India has 398 projects/66,636 rooms in the Pipeline at the end of Q4 2009. The development cycle in India started much later than in China, and existing hotel supply is much less saturated. As a result, the country�s economic strength and growth potential are now attracting increased attention from global hotel companies. Several, including ACCOR, Hilton, InterContinental, and Marriot, already have extensive development programs underway, particularly for their upscale and mid-market brands. The focus is on the large commercial centers. 45% of India�s Pipeline projects and 49% of rooms are currently Under Construction and will accelerate New Hotel Openings through the next two years. In 2010, 78 new hotels/13,709 rooms will enter as new supply. 2011 is forecasted to remain historically high as well, when 74 hotels/11,910 rooms are expected to open. LE�S Forecast for New Hotel Openings

Southeast and other Asia Pacific areas In Q4, the Southeast Asia Pipeline has 251 projects/57,409 rooms, while the rest of Asia has 85 projects/16,267 rooms. With some exceptions, like Thailand, Vietnam, Indonesia, and Malaysia, the economies of most nations in these areas have been dramatically impacted by the global recession. Pipeline declines have been significant and more in line with those seen in other countries worldwide. Construction Starts are in a low channel, as financing difficulties continue to hinder project migration up the Pipeline toward construction. NPAs into the Pipeline remain at low levels. Meanwhile, New Hotel Openings are forecasted to be at cyclical highs in 2010 and 2011. The declining trends in these metrics will combine to erode total Pipeline counts even further through the middle of the decade. © Lodging Econometrics 2010 Lodging Econometrics (LE) is the foremost source of global lodging real estate intelligence for hotel franchise companies, management groups, investment firms, consultants, and vendors to the lodging industry. The Asia Pacific Construction Pipeline Report surveys development for the three stages of construction, three-year forecasts for new hotel openings, two years of prior new openings, and for current supply. Summaries are provided for planning and analysis for the top markets, by chain scale and size of hotel, with comprehensive competitive set intelligence for the leading hotel companies and brands. To order LE�s complete report on the Asia Pacific Construction Pipeline or to inquire about any of LE�s other lodging real estate reports, please fill out the following inquiry form and fax it to LE or contact us at 603-431-8740 x25 or [email protected]. |

| Contact:

Lodging Econometrics

|

| Also See: | Asia Pacific Hotel Construction Pipeline / Q1 2009 / June 2009 |