By Jim Butler

21 May 2009

Here are the insights provided by hotel industry leaders at Meet the

Money® 2009 on the issue of "recovery".

| "We look for a serious recovery in 2011. Then the question is how long

will it take to get back to where we were. Appraisals are forward looking.

We typically build in a rebound - first in occupancy, and then in rate.

We are projecting a 5-year recovery now, and in some properties a 6-year

recovery. It was 7 years in the 1980s. But it will be market by market

and property by property." / Suzanne R. Mellen CRE MAI Managing

Director HVS International |

| LIIC's recent survey of members indicates the majority believe that

lodging real estate investment will get worse before it gets better. The

recession will last up to 18 months or more and hotel values will continue

to decline. / Michael Cahill, CRE, MAI, FRICS, CHA CEO and Founder

HREC |

| "What is the "new normal"? We don't expect to get back to 2007 levels

until the next cycle after the first recovery from now."/ Henry Vickers

Director AEW Capital Management LP |

| "The problem is asymmetrical information which causes a fundamental

disconnect between lenders and borrowers, and gives them very different

expectations. Lenders are getting information in arrears. They are not

even getting pace reports. They don't see what is happening now and going

forward. They are always a month or two behind what is going on. So here

we are in May 2009, and lenders are maybe getting reports on March or April.

They probably are not even getting a revised forecast. This is "Asymmetric

Information." Until lenders have same view of market as borrowers, there

will be no resolution of the markets." / Jonathan Falik Chief Executive

Officer JF Capital Advisors |

| "At the Real Estate Roundtable a couple weeks ago, Bernanke addressed

the group. He seems very smart and listens a lot. He said, " You will begin

to see things get better in weeks -- not months." He said that in October,

our financial model almost fell off a cliff. We are not falling off the

cliff any more. That is positive." / Thomas Corcoran Chairman of

the Board Felcor Lodging Trust Incorporated |

| "We will see RevPAR increases within 6 months after GDP pops, consumer

confidence increases." / Jonathan Falik |

| Housing defaults are still not at Great Depression levels yet (10%)

but we are getting there. Our 90-day delinquency rate is about 7%. There

is a lot of stress on households. Contributing to the stress is household

debt to GDP, which was 40% after WWI, going up to 60% in 1980. This was

acceptable because rent was just another household expense. But after 1980,

household debt to GDP has skyrocketed and is now over 100%. So we will

not see the consumer driving the economy any time soon. / Richard Green

Director USC Lusk Center for Real Estate |

| Beware of false bottoms! Things are still getting worse in the economy.

This is not the bottom. There are more shoes to drop. RevPAR declines are

severe. They have not bottomed and the hotel industry has not bottomed

yet, either. In fact, we have not stopped the accelerated decline. The

3-month moving average will go down for April. Maybe it won't go down quite

as much in May, but it will still be bad. And there is more. The continuing

increased supply problem is not over, but the worsening demand issue is

debilitating. Smith Travel Research likes to use a slide with light at

the end of the tunnel. David uses this one and asks, "Is it light at the

end of the tunnel, or is it an oncoming train?" / David Loeb Managing

Director RW Baird & Co |

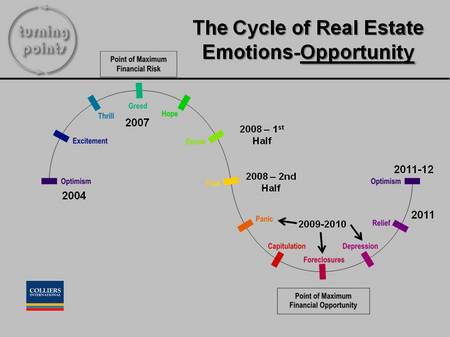

Mark Woodworth, President of PKF Hospitality Research

This chart shows the PKF projections on where we are in the hotel cycle

of emotions and opportunity. We are in a period of capitulation foreclosures

and depression that will last through 2010, with relief beginning to appear

in 2011, and optimism coming only in 2011 or 2012. This slide emphasizes

that the time of greatest financial opportunity is in 2009 and 2010!

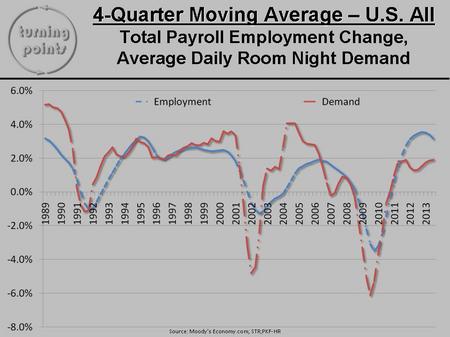

As measured by a 4-quarter moving average, employment and hotel room

demand do not start positive growth until 2011.

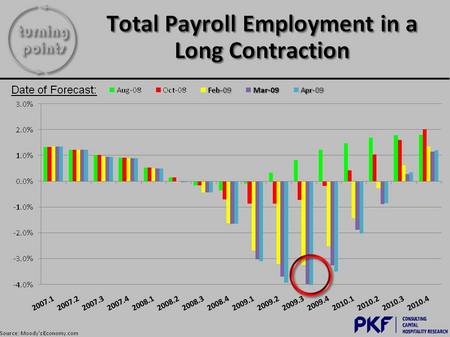

PKF projects that the employment levels affected by current recession

will not return to pre-recession levels of Q4 2007 for 15 quarters. They

will not return to pre-recession levels until Q1 of 2012.

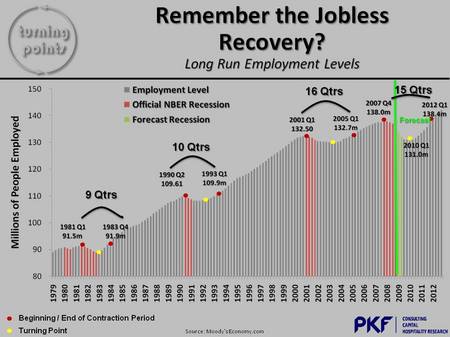

We are not projected to hit the bottom of employment levels until Q1

of 2010, when employment levels will have decreased by more than 7 million

jobs. Many more jobs will be lost before they turn around, roughly a year

from now in April 2010, when unemployment peaks at 9.8%.

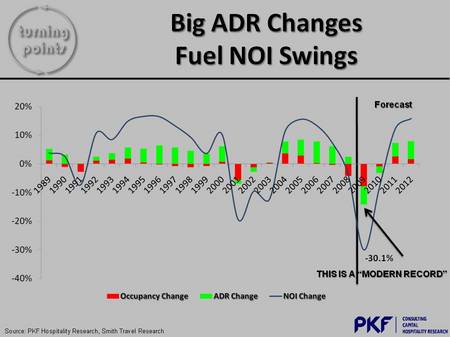

Big ADR declines will set any "modern record" in NOI declines for the

hospitality industry as shown in this chart. This will be the first time

since 1936 that NOI was down 30% or more. In part this is because of the

confluence of 3 factors

Mark Woodworth points out that there have been 122 recessions around

the world between 1960 and 2007. Only four of those 122 recessions had

all three of the following factors:

1. Credit crunch

2. Housing price bust

3. Equity price bust

Mark calculates that with all three of these depressing conditions,

GDP declines are 2 to 3 times greater.

When do we get out of this mess?

I don't know. But there is a lot of pain to endure before we get back

to what we thought was normal. We do believe that the next 12-18 months

represent the greatest buying opportunity in our lifetime, and that it

may well be a long time (7 years or more) before we get back to 2007 levels

of profitability and value, on an inflation-adjusted basis. We hope it

is sooner.

Jim Butler is a founding partner of JMBM and Chairman of its Global

Hospitality Group®. Jim is one of the top hospitality attorneys in

the world. GOOGLE "hotel lawyer" and you will see why. JMBM's troubled

asset team has handled more than 1,000 receiverships and many complex insolvency

issues. But Jim and his team are more than "just" great hotel lawyers.

They are also hospitality consultants and business advisors. For example,

they have developed some unique proprietary approaches to unlock value

in underwater hotels that can benefit lenders, borrowers and investors.

(GOOGLE "JMBM's SAVE program".) Whether it is a troubled investment or

new transaction, JMBM's Global Hospitality Group® creates legal and

business solutions for hotel owners and lenders. They are deal makers.

They can help find the right operator or capital provider. They know who

to call and how to reach them. |