|

|

|

|

|

|

|

Implications for Corporate Structure |

Professor Paul Phillips, August 2003 Introduction The selection of effective capital expenditure projects is cardinal in any efforts to enhance shareholder value. Hence, full appreciation of the relationship between hotel chain capital expenditure (capex) and investment returns is essential. However, the analysis of hotel chain capex has only received cursory mention in previous research studies. Historically, hotel capex studies have converged into two areas: (i) capex techniques with a focus on the utilisation of commonly used capital budgeting techniques; such as net present value, internal rate of return, payback and cash yield on cost and (ii) capex at the hotel unit level with a focus on the amount spent to remain competitive. This briefing has three aims: (i) to identify current hotel capex issues; (ii) to empirically identify salient quantitative and qualitative capex issues within hotel chains; and (iii) to provide directions for future research. Current Capex Issues As the dynamics of the hotel industry gets more complex, there are some important challenges associated with capital spending. Previous hotel capex studies have identified three significant themes, these relate to:

According to Schmidgall, Damito and Singh (1997) hotel industry executives have yet to achieve consensus on the criteria for identifying capex. A major problem within the hotel industry (and other commercial sectors) is the definition of capex (International Society of Hospitality Consultants, 2000). In their empirical study, Schmidgall, Damito and Singh (1997) found that there was strong desire among participants for guidelines that would help hotel industry financial executives determine whether expenditure is capital in nature. Empirical studies have also adopted varying approaches to quantifying hotel capex. For example, KPMG (1999) defined capex as the expenditure in the year that is capitalised in the balanced sheet as fixed asset expenditure but excluded new hotels built or acquired. In the International Society of Hospitality Consultants (2000) study, capex was defined as all of the capital improvement costs of owning hotels over an asset�s life span, including such capital costs that prolong the economic life of the asset. Furniture, fixtures and equipment (FFE) reserve In general, the area of reserves for replacement is another problem within the hotel industry (International Society of Hospitality Consultants, 2000).The amount of reserves that should be set-aside for capital expenditure can create a rift between stakeholders with different interests. Providers of finance and/or lenders wish to ensure that owners set aside more monies (in the form of reserves) to fund capital expenditure, which would reduce the equity investor�s return on investment. Moreover, operators are often held accountable only for operating expenses and would rather capitalise expenditure, and owners would rather expense an item. Within the hotel sector the rule of thumb for the level of repairs and maintenance, is approximately 3-4% of hotel turnover. However, given the declining revenues of some of the major hotel chains, FFE accounts are now shrinking, which make the capital allocation decision all the more intricate. Denton (1998) contends that asset management can be used to forecast capital expenditure and to establish an appropriate schedule of revenue set-sides. It is argued, that setting aside a �standard� percentage of revenue for replacement, may not be an efficient approach to capital reserves. Changing ownership structures In terms of ownership patterns in Europe, the owner-operator model remains applicable to about 71% of European hotels. Jones Lang Lasalle Hotels (2002) have noted the changes in ownership structures and suggested a variety of reasons, including:

Turnover leases and management contracts with guarantees are the top two operating contracts adopted by European pure hotel investors (Jones Lang Lasalle Hotels, 2002). Interestingly, some pure hotel investors companies, such as Hospitality Europe BV have traditionally preferred to acquire hotels operated under management contracts. Hospitality Europe BV is the largest independent hotel owner of upscale hotels in Europe with 8 hotels with 3,230 rooms. Hospitality Europe BV, have adopted a business model to develop or acquire and then redevelop top quality hotels. The business model was evidenced in the case of two hotels in Amsterdam, the five-star Hotel Pulitzer and the five-star Sheraton. After development work was complete both properties were put up for sale in September 2002. Management wished to execute the original business model and return cash to shareholders. Current and future owners of hotel properties want to maximise the utility derived from capex, which is equivalent to maximising return, in an increasingly demanding global business environment. The Capex Study Methodology The Chief Executive Officer and/or Chief Financial Officer of seven major international hotel companies were interviewed about quantitative and qualitative capex issues within their group. The research instrument had two parts. The first part asked for quantitative data with a focus on maintenance and development capex. The second part was designed to obtain qualitative information about property and corporate structure capex. Findings Property capex General: According to the Hotel Association of New York City in their Uniform System of Accounts for the Lodging Industry (1996 p26) �a separate disclosure (on capex) may be appropriate for the portion of the capital expenditures that results in an increase in the revenue-generating capacity of the lodging property. Separating cash payments that represent an increase in revenue-generating capacity from cash payments that are required to maintain operating capacity is helpful in enabling users to determine whether the lodging property is investing adequately in the maintenance of its operating capacity.� Also, the Uniform System of Accounts for the Lodging Industry (1996 p9) defines depreciation as �� a method of allocating the net cost (after reduction of expected salvage value) of the individual assets or classes of assets to operations over their anticipated useful lives.� The relationship between maintenance capex and depreciation provides an indication of any possible adverse affect on property value. Interestingly, some participants� total maintenance and development capex were less than the depreciation charge. Participants stated that the main reasons for capex was generally for introduction of new hotels, expansion of existing facilities, replacement or improvement of existing facilities. However, there were some differences of opinion regarding the treatment of capex with regards to repairs and maintenance and reserves for replacement. For example, some hotel general managers were keen to use reserves to fund the replacement of major building components such as lifts, instead of using reserves for the periodic replacement of FFE. There were two approaches to capex spending. First, there was the big bang approach, which was funded by a build up of reserves for replacement over a period of time. Secondly, there was an incremental approach, where capex was spent in relatively small amounts over a period of time. Some participants mentioned that the latter approach was an inconvenience to the customer. Maintenance: Among the sample it was felt that an effective maintenance capex policy should be preventative rather than reactive. To be placed in a catch up situation with competitors was to be avoided. Figure 1 shows that the 4% rule of thumb measure for maintenance capex does not reflect current hotel chains practice. The disparity in the maximum and minimum levels of maintenance capex, as a percentage of hotel owned and leased turnover was evident. On the one hand, during 2002, one hotel chain spent 20.9% of its hotel owned and leased turnover on capex, while the least amount spent by one hotel chain was 3.1%. Figure 1 Maintenance Capex

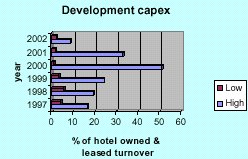

In terms of maintenance capex per owned and leased room for 2002, the figure peaked at £6,259 with the lowest amount spent being £725. Despite the fact that the two hotel groups targeted different market segments and had a much different geographical coverage, the discrepancy raises some intriguing issues. Figure 2: Development Capex

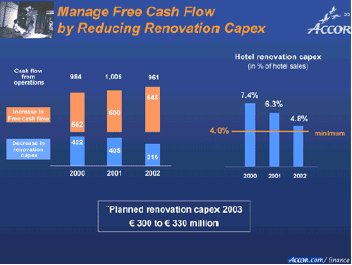

Development: Hotel companies have never been more profitable than they were in 2000, so it was not surprising that capex peaked in the same year. As shown in Figure 2, there was divergence in the distribution of development capex, as a percentage of hotel owned and leased turnover. For example, one hotel chain recorded a development capex peak of 51% of hotel owned and leased turnover in 2000 with a decrease in corresponding figures for 2001 and 2002 of 33.1% and 8.7%, respectively. In 2000, the smallest percentage spent by a hotel chain was 1% of its owned and leased turnover on development capex, with an increase in corresponding capex figures for 2001 and 2002 of 1.7% and 2.2%, respectively. Corporate structure capex IT: Participants made significant efforts to enhance revenue through higher levels of occupancy and customer satisfaction by investing in property management, central reservations together with an array of other IT applications, including customer relationship management. However, as succinctly put by one CEO �Capex can involve upgrading to a corporate system, but whether there is a return is debatable.� Other CEOs wondered if there was a pressure to change for the sake of technology, by the IT department, rather than enhancing the financial return. IT was seen by some organisations as an enabler rather than the driver of e-business. Some interviewees mentioned the importance of human resources, and stressed that capex should address IT infrastructure issues (e.g. organisation structure, process and people), as well as technology related issues. It was felt by some that IT was really being used to increase the convenience to customers, with IT being treated merely as a cost of doing business. A useful case in point is e-business, where in some hotel chains the level of online bookings is small. However, despite hotel chains spending significant sums of capex on e-business, the amounts being spent were minute when compared to amounts spent by online travel agents. For example, the $1.1 billion transaction by USA Interactive (now InterActiveCorp - www.IAC.com) completed in June 2003, to acquire the outstanding shares that it did not currently own in Hotels.com illustrates the level of investment being made by Internet third-party intermediaries. Hotels.com is the largest specialised provider of discount lodging 8 worldwide. During, the six year period 1997 to 2002 Hotels.com sales turnover grew from $35m to $945m, which represents a growth of 2,600%. However, according to Hotels.com, their share of the global lodging market at the year end 2002 was less than one-third of 1%. Moreover, according to their estimates $120 billion worth of empty rooms annually exist in the USA and European lodging markets. Brand infrastructure: Significant amounts were being spent on a well-defined corporate and brand infrastructure. One hotel chain spent approximately 15% of hotel turnover on corporate and brand infrastructure. A key lesson learned by some was the necessity to focus on the cost of investing in the brand change during expansion into new markets. For example, some participants mentioned that as the hotel unit in the UK tended to be older than its US counterpart, the cost (per room) of the brand change was higher in the UK. So, it was necessary to spread the cost of upgrading the brand standards of (e.g. locks on doors, fire and smoke alarms, etc.) over a time period, which in some cases was ten years. It was also noted that the criteria and measurement of success of corporate capex was not clear. This lack of criteria and metrics for corporate capex accomplishment should be borne in mind, as the more hotel companies are involved in management contracting and franchising, the more capex is corporate rather than hotel capex. Moreover, both the 2003 and 2002 annual BusinessWeek brand surveys conducted with Interbrand, which ranks 100 global brands that have a value greater than $1 billion contains no hotel chain. The absence of a hotel chain among BusinessWeek�s top 100 global brands for the last two years (the Hilton brand was positioned 96 th out of 100 th in 2001) demonstrates the necessity for a clearer understanding of the link between hotel chain brand infrastructure and profits. Investment strategies: The recurring nature of economic cycles makes it imperative for companies to time their capex in order to exploit their returns. In compliance with conventional thought, participants felt that the bottom of the cycle was a good time to invest, as hotel companies were in strong negotiating position with all parties involved in the hotel development process. However, when there is a slowdown in earnings growth, shareholders become more watchful of returns. Management have to seek a balance between distribution (e.g. where does the surplus capital get deployed � on the property or to the shareholder?) As failure to ascertain the appropriate balance in distribution could affect the share price. In a downturn environment, those hotel companies without deep pockets have had to cut back capex to sustainable amounts with the emphasis on maintaining the estate. For example, Accor in their 2002 full-year presentation to analysts (see Figure 3) illustrated how they achieved their desired free cash flow from operations by decreasing renovation capex, from €422m in 2000 to €316m in 2002. This contributed to an increase in free cash flow from operations from €562m in 2000 to €645m in 2002. Figure 3: Accor Managing Free Cash flow

Evaluating returns: The importance of the post investment appraisal was stressed, but it was felt that it was a difficult task to perform well. One hotel company did not perform detailed post investment analysis, as it was felt that returns could be affected by too many factors beyond the control of management. In addition, it was difficult to link cause and effect. Nevertheless, in some cases it was relatively easy to gauge success, e.g. adding a footprint to the property portfolio. In replacement and multiphase capex projects, it was difficult to disaggregate investment and returns. In these instances, the focus was on the overall story, picture and track record. However, if these basic indicators go astray, shareholders begin to ask awkward questions. In these instances the �forensic� shareholder can present significant problems to the management team. What's Next? In this briefing we have explored quantitative and qualitative hotel chain capex issues. The selection of good capex projects is cardinal in any efforts to enhance shareholder value, so in theory, property capex and corporate structure capex should be no exception. Moreover, in difficult business conditions it is even more important for hotel chains to benchmark their capex investment against their peers with emphasis on the property; IT, brand and corporate HQ. The findings from this study suggest that the global hotel industry would benefit from more in-depth quantitative and qualitative hotel chain capex studies relating to: Property

Acknowledgement: The author would like

to express thanks to all the participants

References BusinessWeek (2003) The top 100 brands, special report, August 4-11, European Edition, 48-51. Denton, GA (1998) Managing capital expenditures, Cornell Hotel and Restaurant Administration Quarterly 39(2) April, 30-37 Hotel Association of New York City, Inc (1996) Uniform System of Accounts for the Lodging Industry, Educational Institute of the American Hotel & Motel Association, Michigan, East Lancing. International Society of Hospitality Consultants (2000) CapEx 2000, A study of capital expenditures in the US Hotel Industry, Alexandria, VA. Jones Lang Lasalle Hotels, (2002) Changing ownership structures, December, Issue 13, London. KPMG (1999) Capital expenditure: a survey of UK hotels -1998, London. Schmidgall, RS, Damitio, JW and

Singh, AJ (1997) What is capital expenditure? Cornell Hotel and Restaurant

Administration Quarterly 38(4) August, 28-33.

|

| Contact:

Professor Paul Phillips Charles Forte Chair of Hotel Management Email: [email protected] Tel:+44 (0)1483 686319 http://www.som.surrey.ac.uk/ |

| Also See: | ISHC Releases CapEx 2000 - A Study on Capital Expenditures in the Hotel Industry / Oct 2000 |