|

. INNvestment Canada Third Quarter 2003 |

|

|

More Prosperous Times Balancing Supply and Demand Growth in room-night demand has slowed during the past four years for a number of uncontrollable factors - September 11 th , general economic malaise, the ongoing instability in the Middle East including the Iraq War, airline bankruptcies, the SARS outbreak and the Mad Cow scare. Perhaps these issues have kept us from reasonably exploiting the growth area we can control - new hotel supply.

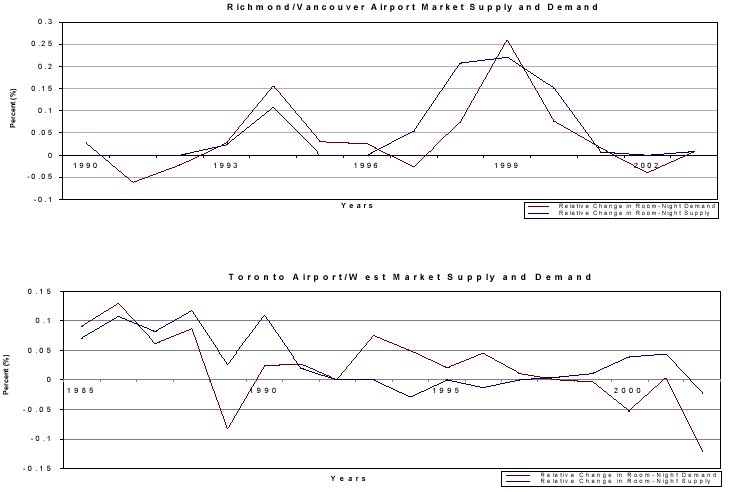

Prudent owners and developers may want to revisit past trends in markets where lodging fundamentals have been permanently altered by oversupply issues. Did we not learn from the Richmond/Vancouver Airport market in the late 1990s? With the market enjoying occupancy levels in the 75% to 80% range for almost a decade, new hotel construction was inevitable. In a three-year period (1997 to 1999) nine new hotels opened, plus an existing hotel expanded, increasing the room inventory by almost 1,900 rooms, or 77%. By the bottom of the cycle, market occupancy reported in 2000 had dropped to 65%. The good news � less than 150 rooms have since entered the market and only the 50-room La Quinta Inn Vancouver Airport is under construction. The bad news - the market occupancy now sits below 65%.

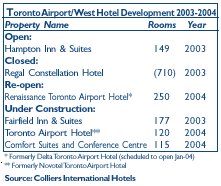

It wasn�t until 1993 when the surge in new development in the Toronto Airport/West market ceased and occupancy stabilized at sub 60% levels. It took another five years during which time demand grew at a compound annual rate of about 4% and supply contracted by 418 rooms for occupancy to return to the 75% range enjoyed a decade earlier. More than 80% of new hotels being developed are affiliated with a brand. The most active hotel brand during the past five years was Super 8 Motels, adding approximately 2,900 new rooms. Other active brands include; Holiday Inn with some 1,800 new hotel rooms, Hampton Inn reporting an estimated 1,400 new rooms and Days Inn with about 1,300 new rooms, and Courtyard by Marriott and Delta Hotels both reporting approximately 1,000 new rooms. Despite improved economic conditions (Toronto�s GDP grew by 6.9% in 1999 and 5.5% in 2000) room-night demand began to slowly contract after 1998. This was further compounded by the steep decline in corporate and leisure travel to Canada that started in Q4 2001. By the end of 2003, we estimate room-night demand will have declined by more than 15% since its peak, matching levels comparable to the early 1990s. Notwithstanding the closure of the Regal Constellation Hotel (710 rooms) and the former Delta Toronto Airport Hotel (250 rooms), occupancy is still tracking for a substantial decline in 2003. Based on year-to-date results and forecasts published by HVS International and PKF, and our knowledge of the market, it is quite likely occupancy within market below 60% by year-end. Why then are so many proposed hotels rumoured for this market? There are about 800 new rooms that will open by the end of next year. Beyond 2004 will be anyone�s guess, but the industry as a whole needs to be cognizant of the repercussions of supply growth outpacing demand, particularly when occupancy falls below the 60% level. We are presently aware of eleven proposed hotels in the Toronto Airport/West market, representing a total of 1,750 rooms, including the re-opening of the Delta Toronto Airport Hotel as the Renaissance Toronto Airport Hotel and the anticipated re-opening of the Regal Constellation Hotel under new ownership. For the most part, these projects are being sponsored by owners/developers that have a demonstrated propensity towards new-builds versus acquiring existing product. Even if 50% of these projects come to fruition over the next three to four years, demand will need to increase by more than 10% to surpass supply growth and improve occupancy. While these new hotels will likely be successful, existing owners with older hotel product will need to commit substantial capital to maintain their assets at competitive levels. |

| Hotel investment activity slowed in Q3 2003 with some $59.7 million

of transaction volume reported nationally, compared to Q1 and Q2 when approximately

$64.7 million and $170.4 million of transaction volume occurred, respectively.

Third quarter 2003 is also below Q3 2002, when approximately $175.0 million

in transaction volume was reported ($100.0 million of which were strategic

acquisitions).

Transaction volume year-to-date (YTD) September 2003 reached approximately $294.7 million at an average value of $65,600 per room, with the sale of 35 hotels. Five provinces reported activity, with twelve trades in Ontario ($103.8 million), eight in British Columbia ($45.6 million), eight in Alberta ($73.1 million), four in Saskatchewan ($8.5 million) and three in Quebec ($63.7 million). While there have been no strategic trades in 2003, there has been a diverse range of hotel product sold, from small inns such as the $5.7 million sale of the 23-room Abigail�s Hotel in Victoria, to the sale of full-service, urban hotels like the 721-room Toronto Colony Hotel in Toronto for $67.0 million and the Renaissance Montreal Hotel for $29.95 million. The most significant trade this quarter was the sale of the Sheraton Grande Edmonton Hotel. This 313-room, city-centre hotel sold in September 2003 to Sutton Place Grande Hotels Group for $17.0 million ($54,300 per room). Although transaction activity decelerated in the third quarter, it is anticipated investment activity will be strong for the remainder of the year. The fourth quarter began with the acquisition of FelCor Lodging Trust Incorporated�s Ontario Hotel Portfolio (properties located in Peterborough, Sarnia, Kitchener and Cambridge) by Fortis Properties Corporation for an aggregate price of $43.2 million ($68,700 per room).

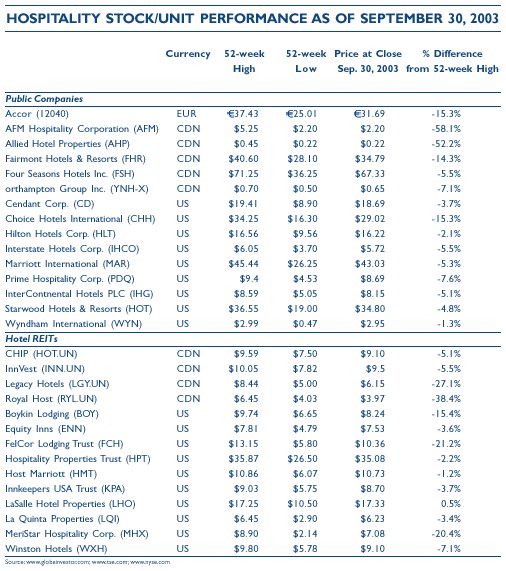

The Stock Market Watch Lodging stocks continued to show decreases at the end of the third quarter 2003. Each public company on the stock list below reported a decrease in performance with the exception of Lasalle Hotel Properties, which closed 0.5% higher then their 52-week high at $17.33. AFM Hospitality Corporation showed the biggest decline, closing the quarter at $2.20, 58.1% below its 52-week high at $5.25.

|

|

Leaders in Commercial Real Estate Since 1898 Offering clients a full range of real estate services in over 251 markets worldwide INNvestment is published quarterly by Colliers International Hotels. Comments and suggestions are welcome |

###

|

Colliers International Hotels Hotel Investment Advisory Services Bill Stone Alam Pirani Deborah Borotsik Sylvia Occhiuzzi [email protected] One Queen Street East Suite 2200 Toronto, Ontario M5C 2Z2 Phone: (416) 777-2200 Fax: (416) 777-9232 http://www.colliershotels.com |

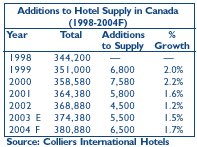

Nationally,

supply increased at a compound annual rate of about 1.4% between 1998 and

2002, from an estimated inventory of approximately 344,200 rooms in 1998.

Going forward we estimate 5,500 hotel rooms will open in 2003, with another

6,500 rooms under construction or in the planning stages that are slated

to open in 2004. On the demand side, PKF reported a compound annual growth

of only 0.5% during this period � well below the growth in supply. Over

the past few years, this supply and demand imbalance caused the national

occupancy to fall by almost 8%, from 67.0% in 1998 to an estimate of only

59% in 2003.

Nationally,

supply increased at a compound annual rate of about 1.4% between 1998 and

2002, from an estimated inventory of approximately 344,200 rooms in 1998.

Going forward we estimate 5,500 hotel rooms will open in 2003, with another

6,500 rooms under construction or in the planning stages that are slated

to open in 2004. On the demand side, PKF reported a compound annual growth

of only 0.5% during this period � well below the growth in supply. Over

the past few years, this supply and demand imbalance caused the national

occupancy to fall by almost 8%, from 67.0% in 1998 to an estimate of only

59% in 2003.

Although

new hotel construction is not a primary concern in all markets, there are

pockets that developers need to proceed cautiously - a prime example is

the Toronto Airport/West hotel market (Greater Airport Area). Our review

of historical supply and demand trends showed that double-digit demand

growth and controlled increases in supply pushed occupancy to almost 75%

between 1986 and 1988. As in Richmond, these conditions appeared to justify

hotel construction. Six new hotels, with an aggregate of 1,100 rooms opened

in 1986 and 1987, and another eleven hotels, representing almost 2,900

rooms, entered the development-planning pipeline. In hindsight, we now

know demand growth was about to slow considerably and even contract by

a staggering 8% in 1990 as the economic recession hit the hospitality industry.

Although

new hotel construction is not a primary concern in all markets, there are

pockets that developers need to proceed cautiously - a prime example is

the Toronto Airport/West hotel market (Greater Airport Area). Our review

of historical supply and demand trends showed that double-digit demand

growth and controlled increases in supply pushed occupancy to almost 75%

between 1986 and 1988. As in Richmond, these conditions appeared to justify

hotel construction. Six new hotels, with an aggregate of 1,100 rooms opened

in 1986 and 1987, and another eleven hotels, representing almost 2,900

rooms, entered the development-planning pipeline. In hindsight, we now

know demand growth was about to slow considerably and even contract by

a staggering 8% in 1990 as the economic recession hit the hospitality industry.