|

|

|

|

|

|

|

|

|

| By Harry Madhoo,HVS International

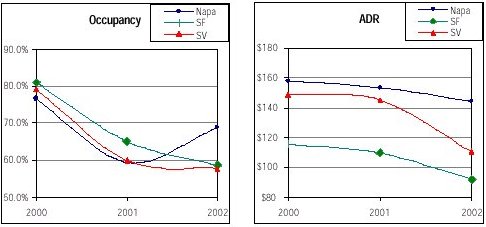

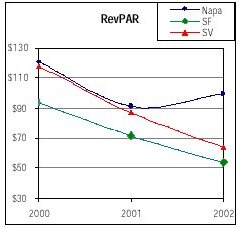

May 2003 In August 2002, the San Francisco office of HVS International published profiles of several hotel markets in the state of California including San Francisco (SF), Silicon Valley (SV), and Napa, among several others. This article updates and contrasts the performance of the Napa and Silicon Valley submarkets, which we believe represent the two ends of the spectrum insofar as hotel performance in the San Francisco Bay Area is concerned. For information purposes, we have also presented data on the performance of the San Francisco market. Historical Trends The following charts summarize the performance of the three submarkets in terms of occupancy, average rate (ADR) and revenue per available room (RevPAR). While the data pertains to selected samples of hotels reporting to Smith Travel Research in each submarket, they do nevertheless provide an overall indication of general supply and demand dynamics, as well as trends in ADR and RevPAR in those submarkets.

Source: Smith Travel Research and HVS International . The trends indicate that Napa has been the most resilient of the three submarkets. In 2002, Napa was the only submarket that experienced an increase in occupancy over the prior year�s performance, an increase from roundly 60% (2001) to roundly 70% (2002). The market experienced an increase of roundly 28% in demand, which more than offset the 11% increase in supply (the 85-room expansion of the Marriott Napa Valley in August 2001 and the opening of the 80-room Hilton Garden Inn in September 2002). Unlike Napa, both San Francisco and Silicon Valley experienced further declines in occupancy in 2002, albeit more moderate declines when compared to those of 2001. All three submarkets experienced further declines in average rate in 2002: roundly $10 for Napa; $18 for San Francisco; and $34 for Silicon Valley. As indicated, the magnitude of the decline (both in dollar and percentage terms) was smaller for the Napa submarket, compared to those of San Francisco and Silicon Valley. Overall, in 2002, San Francisco and Silicon Valley experienced declines of roundly $18 and $23 in RevPAR, respectively; by contrast Napa experienced a RevPAR increase of roundly $10 in 2002, which further reinforces the resilience of the Napa submarket. Nature of Demand The contrasting fortunes of these three submarkets is closely correlated with nature of the demand. While the Napa hotel market derives a large portion of its guestroom demand from throughout the greater San Francisco Bay Area, Napa is a predominantly leisure market, with an estimated segmentation of roundly 60% leisure, 20% commercial, and 20% meeting and group demand. As the �Food and Wine� capital of the nation, Napa is a regional and national destination, attracting visitors from major metropolitan areas, especially more so from cities within reasonable driving distances. Historically, Napa Valley visitation has been strong during good economic times and proven to be very resilient during the recessionary years of the early 1990s. During that recession, people traveled less and took driving trips close to home. Napa Valley benefited from this trend and is currently experiencing a similar demand pattern, with weekends experiencing strong drive-in leisure demand. By contrast, the Silicon Valley submarket (as represented by our sample

of hotels) is predominantly commercial in nature, with an estimated segmentation

of roundly 75% commercial, 15% meeting and group, and 10% leisure demand.

Additionally, most of the meeting and group demand is commercial in nature.

Major demand generating companies in the market include Agilent Technologies,

AT&T, Novell, Cisco Systems, Siemens, Sun Microsystems, General Motors/Toyota,

New United Motor Manufacturing Inc., Cirrus Logic, Lam Research, Hewlett

Packard-Compaq,

In summary, both Napa and Silicon Valley are heavily dependent on one demand segment: leisure demand for Napa and commercial demand for Silicon Valley. Unlike Silicon Valley, the Napa submarket has proven to be much more resilient primarily to due its reputation as the �Food and Wine� capital of the nation and its ease of access by automobiles from surrounding metropolitan areas. Additionally, Napa Valley experienced much less increase in supply between 1999 and 2002; Napa Valley remains a highly desirable market for developers; barriers to entry are high mostly due to a lack of suitable development sites and lengthy approval/entitlement processes. |

| Contact:

116 New Montgomery Street, Suite 620 San Francisco, CA 94105 |