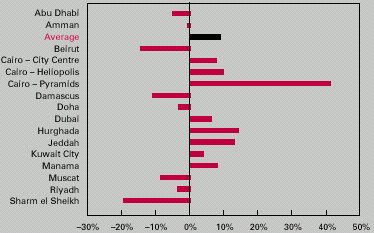

| The recovery of the region�s economies and the relative stability in

the region ensured that the aggregate average rates increased by approximately

4% between 1999 and 2000. We would draw the reader�s attention to Table

7, which indicates the positive growth shown by all of the destinations

surveyed in Egypt. This growth came in spite of strong increases in supply

and shows the resilience and continued popularity of the country.

It is our opinion that average rates are likely to show some level of

decline in 2001 as supply increases and the Middle East economies show

a slight downturn. We would also highlight that the region is facing increasing

competition from destinations such as North Africa and Asia where increasing

supply and economic downturns have forced prices downwards.

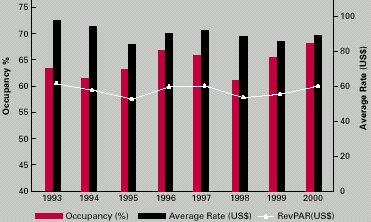

RevPAR in the region rose to US$60, one of the highest levels in the

last decade, an increase of approximately 8% on 1999 levels. The main driver

of this increase has been the recovery of oil prices and relative stability

in the region during 2000. It is our opinion that RevPAR levels may decline

over the next few years due to increases in supply and tensions in the

region; however, the longer term outlook is positive with the region committed,

in the most part, to continuing to improve its image and attract increasing

levels of visitors over the coming years.

Country Analysis

Bahrain

In common with Dubai, Bahrain has had to compensate for its relative

lack of oil by establishing itself in other fields, and building for the

mid- to long-term future. By preference Bahrain has set out to target the

business travel sector, most notably the exhibition, conference and incentive

travel market. The estimated GDP growth for 2000 was exceptionally high

in Bahrain at 5.2%. This growth was due to the recovery in Asia and to

the increasing reputation of Bahrain as a commercial centre for the Gulf.

Bahrain has embarked on a 50-year plan to develop additional land area

and create artificial islands. This increase in land should allow Bahrain

to satisfy the requirements of the leisure and recreation sectors.

As predicted in our study last year, 2000 was exceptionally good for

the hotel industry in Bahrain and annual levels of profitability for the

quality hotels have increased significantly due to an increase in both

occupancy and average rate. Occupancy levels in

Manama increased by three percentage points in 2000 to 59%, making some

headway in recovering from the decrease experienced during the previous

two years. The lower midweek occupancy has been compensated for by the

influx of Saudi traffic during the weekends as Bahrain has the reputation

of being an ideal family destination for Saudi nationals. Average

rates rose from US$102 in 1999 to US$105 in 2000, an increase of approximately

3%.

Bahrain has redeveloped its strategy for tourism and the general mood

amongst the hoteliers is currently buoyant. The Sheraton, the Inter-Continental

and Diplomat hotels (the last, following the signing of its recent management

contract with Radisson SAS) are all part of the way through major refurbishment

programmes. In terms of new developments, Accor has confirmed that it is

to open a new 180- room Novotel near to the beach. Other operators have

expressed a desire to move into the market. We have also identified some

larger tourism master plans outlined for future development in Bahrain

such as the Al Dana Seaside Resort, a US$26.5 million development on a

34,000 m 2 site near the Marina Club. The most ambitious plan is Durrat

Al Bahrain, a new US$795 million resort development. It is our opinion

that, in the short term, the hotel sector will continue to improve its

occupancy and average rate performance as the country becomes increasingly

attractive to both commercial and leisure visitors.

Egypt

For the first time since President Mubarak took office, the government

isnow committed to increasing foreign investment and generating employment.

Despite a current background of heightened regional tensions as the Middle

East peace process falters, the economic outlook for Egypt is favourable.

Inflation is officially recorded at below 10% with the budget deficit below

2%, largely because of cuts in subsidies.

Tourism to Egypt has continued to show strong growth with tourist arrivals

in 2000 above the 5 million mark for the first time ever: a 7% growth when

compared to 1999. We would comment that while growth has been positive,

the air transport infrastructure is still inadequate. If growth is to continue,

then major investment will be required with respect to airport facilities

in addition to an increase in scheduled flights from European destinations.

Cairo City Centre, with only a limited increase in supply, continued

to show strong growth, particularly in terms of average rate. While occupancy

levels remained stable at 78%, the second-highest recorded in our survey,

average rates increased by approximately 7% to US$86. This average rate

is the highest achieved in Cairo City Centre since 1995. Furthermore, strong

growth was also recorded for hotels located in the Heliopolis area. Occupancy

levels remained stable at 83%, the highest recorded in our survey, and

average rates increased by approximately 9% to US$68. With strong levels

of demand in the city centre and increased commercial activity in Giza,

hotels near to the Pyramids also showed strong growth in both occupancy

and average rate. Our research indicates that occupancy levels increased

six percentage points to 76%, the highest level since 1993; average rates

increased by a massive 31% to US$66.

These strong increases in average rates can be attributed to stable

levels of supply and strong demand from commercial, meeting and conference,

and leisure segments which ensure that Cairo hotels typically achieve some

of the highest occupancy levels in the Middle East.

However, a number of new hotels are planned to open in the near future

in Cairo City Centre, Heliopolis and the Pyramids areas. Near to Heliopolis,

a 425-room JW Marriott is currently under construction. The hotel will

feature extensive meeting facilities, as well as world class spa and leisure

facilities, including a golf course. We are also aware of a 194-room Holiday

Inn which is to be developed in the Heliopolis area. In terms of city centre

hotels, the Nile Plaza Cairo Four Seasons is expected to open in 2002,

the second Four Seasons hotel in the city. Further new openings include

a 513-room Hyatt hotel, an 800-room extension to Le Méridien, a

900-room Crowne Plaza and a Kempinski hotel. Developments are also

occurring in the vicinity of the Pyramids at 6 th of October City. These

developments include a 220-room Mövenpick hotel, a 220-room Hilton

Dreamlands Golf Resort and a Novotel.

Hotels in Hurghada recorded an aggregate decrease in occupancy levels

of three percentage points in 2000, to 77%. This decrease was caused primarily

by an increase in hotel supply. However, average rates in 2000 increased

by approximately 20%, when compared to those achieved in 1999, and reached

US$41. Supply continues to increase with the development of the 200-room

Holiday Inn Amphoras (opening in 2001), a 300-room Park Plaza (2001), a

304-room Radisson SAS Dana Beach Resort (2001) and a 405-room Steigenberger

Fanadir Resort (2002). This increase in supply is likely to have a detrimental

effect on operating performances; however, as has been seen in the past,

tour operators are likely to be able to fill these rooms, albeit at increasingly

lower rates.

Occupancy levels in Sharm el Sheikh decreased dramatically in 2000 to

63% from a seven-year high in 1999 of 79%. This decline was again caused

by a dramatic increase in supply, as predicted last year in our Middle

East report.

Some of this supply includes hotels to be managed by Sol Meliá

(two hotels), Le Méridien, Sheraton Four Points (two hotels), Four

Seasons, Crowne Plaza, Swissôtel, Steigenberger and Rotana. We would

also highlight Nabq Bay, a short distance from Sharm el Sheikh, where it

is planned that approximately 8,000 rooms (27 hotels) will be developed

over the next seven years. In addition, there are a significant number

of hotel rooms being built along the coast up to Taba, including hotels

managed by Steigenberger, Hyatt, Sofitel, Marriott and Inter-Continental.

At present, the facilities at Sharm el Sheikh airport are nearing capacity,

and, although government officials have promised that this problem will

be rectified, no discernible action has yet been taken. The continued success

of Sharm el Sheikh and the Red Sea coastline rests largely on the government�s

ability to implement successfully the expansion of the country�s air infrastructure

and indeed to allow an �open skies� policy. We have recently been informed

that plans to upgrade and expand the airport have been approved; however,

no date for this work to commence has been confirmed.

Jordan

Jordan�s geographic location at the centre of the Middle East means

that its fortunes are strongly influenced by regional circumstances. Therefore,

Jordan suffers significantly with the continuing unrest and violence between

Israel and the Palestinian Authority. Trade sanctions with Iraq also continue

to have a negative effect on Jordan�s exports: Jordan has long served as

a transit route for goods destined for Iraq, from where Jordan also received

subsidised oil. Since the UN trade embargo Jordan has been forced to import

oil from Yemen and Syria at higher prices. The service sector is by far

the country�s largest, accounting for approximately 70% of GDP. GDP growth

was approximately 2.5% in 2000 compared to an expected growth of 3.5% as

presented in our report last year. The rate of growth is expected to improve

over the coming years.

The tourism industry is widely regarded as a major potential foreign

exchange earner. The Jordanian government expected strong growth of approximately

20% in terms of tourist arrivals for 2000. However, due to the development

of political tensions in the region in addition to Jordan�s strategy of

marketing itself as part of a multi-destination trip including Israel,

the estimate for 2000 suggests a decrease of 7.5% compared to 1999.

Quality hotels in Amman showed an increase in occupancy levels for 2000

of 59%, compared to 56% in 1999, despite the significant decrease in visitor

arrivals. Average rates fell by approximately 5% in 2000 to US$68, the

lowest level for seven years.

Amman has experienced an increase in supply over the last few years,

including new Hyatt and Holiday Inn hotels and an extension to the Inter-Continental.

Further development in the quality hotel sector is likely to occur in the

next three years with the opening of the Sheraton, Crowne Plaza and Four

Seasons hotels, which are all under construction. The continued tension

between Jordan�s neighbours and this increase in supply are likely to have

a detrimental effect on performance levels in the coming years.

Additional areas for development in Jordan include the Dead Sea coastline.

Openings over the next few years include the 212-room Marriott Dead Sea,

a 240-room Novotel hotel and a 170-room Inter-Continental hotel.

Furthermore, there are a number of projects being developed in Aqaba, including

a 300-room Marriott (planned to open in 2004), a 250-room Mövenpick

and a 1,000-room resort.

Kuwait

For the last half-century, oil has dominated the Kuwaiti economy, and,

with current reserves estimated at around 10% of the world�s total, this

domination does not look like changing in the near future. Due to the huge

level of investment still required to rebuild the country and despite the

highest oil prices for nearly ten years, Kuwait still has one of the slowest-growing

economies in the region.

The Kuwaiti economy, on the surface at least, looks to be in very good

shape, with the budget surplus up and rising oil prices. The economic indicators

in 2000 unfortunately mask sluggish progress in necessary economic reforms.

In 2000, it was reported that 80-90% of arrivals in Kuwait were still

business-related. Some modest attempts have been made to try to promote

Kuwait as a leisure destination, but the facilities and entry procedures

are very much geared towards the business visitor.

Occupancy levels in the five-star properties decreased by one percentage

point to 46%. Average rates increased quite significantly from US$169 to

US$178, the highest in our survey. Although occupancy levels in the

five-star hotels remain very low there are a number of different projects

under construction in the four-star and five-star sector. A 150-room Hilton

located on the beachfront is under construction near Ahmadi, where most

of the oil companies are located. In the city centre a 150-room Four Points,

an 80-room Taj Hotel and a 300-room Courtyard by Marriott are currently

under construction. We have been informed that the redevelopment of the

Messilah Beach is currently on hold.

With a 20% increase in hotel room supply and limited prospects for demand

growth in the near future, occupancy levels are likely to suffer further.

Lebanon

Lebanon experienced a significant economic downturn in 2000 following

the strong growth experienced in the early 1990s. The downturn was caused

by a decrease in private spending with consumers waiting to see the outcome

of reforms in Lebanon in addition to regional peace prospects. The outlook

for Lebanon is somewhat better and forecasts estimate GDP growth at approximately

1.5% and 2.5% in 2001 and 2002, respectively. This growth largely depends

on the new Prime Minister Rafiq al-Hariri and his ability to impose the

government�s reforms on the country�s restless parliament.

Despite the subdued economic growth, tourism has proved to be one of

the few sectors to show continued growth over the last ten years. Visitor

arrivals increased annually by approximately 20% between 1992 and 2000

(albeit from a low base). The proportion of leisure visitors within these

arrivals has increased from approximately 26% in 1996 to 32% in 2000.

Occupancy levels in quality Beirut hotels increased slightly in 2000

by one percentage point to 57%, despite a large increase in supply over

the past few years. Nevertheless, average rates in the market decreased

by approximately 15% to US$110, attributable largely to the poor economic

conditions and the increase in supply with the opening of the Holiday Inn

Martinez and the Phoenicia Inter-Continental. Furthermore, these declining

operating performances have meant increased pressures for those international

hotel companies managing properties; several hotels previously branded

are now being independently operated.

As mentioned last year, the Phoenicia Inter-Continental, the first hotel

in recent times to have large, modern meeting facilities, has indeed begun

to generate a number of regional conferences, which have increased the

exposure of Beirut and generated demand from within a market segment that,

historically, has been relatively weak in Beirut over the last 30 years.

Several hotels are under construction and are due to open in the near future,

including the 280-room Mövenpick Hotel (2002), the 115-room rebranded

/ refurbished Sheraton Coral Beach (2001), the 198-room Crowne Plaza (2001)

and the 225-room Metropolitan Hotel (2001). A Four Seasons hotel, which

is to be located opposite St George�s Marina, is projected to open in 2005.

We have also been informed that the former Hilton hotel is to be pulled

down and reconstructed with a total of 460 rooms. As this new supply

becomes operational, operating performances are likely to decrease. However,

at present, there are only a few international branded, quality hotels

in Beirut with facilities to attract commercial, meeting and incentive,

and leisure guests. The development of these projects in the medium to

long term should ensure that Lebanon becomes a more desirable destination

for both commercial and leisure demand. However, if regional tensions are

not eased, this growth is likely to be severely curtailed.

Oman

Despite continuing uncertainty surrounding the successor to Sultan Qaboos

bin Said al-Said, there are no significant threats to the political order

and Oman is expected to remain stable throughout 2001. Oman has remained

within the Arab mainstream on the region�s most contentious foreign policy

issues, and there are unlikely to be any moves to restore commercial ties

with Israel even if violence in the West Bank and Gaza recedes. The official

net budget deficit will widen as spending picks up and oil revenue eases,

but the domestic position will remain one of surplus. Growth should accelerate

in 2001 despite softening oil prices, as domestic demand picks up and non-oil

exports rise.

Data on visitor arrivals to Oman in 2000 are not yet available; however,

informed reports suggest that these numbers have remained largely stable.

Occupancy levels for Muscat�s quality hotels have decreased marginally

to 55% in 2000, due to the increase in supply experienced over the last

two years in the city. In addition, the general instability in the region

and the increase in supply have caused average rates to decrease by approximately

5.5% to US$86.

There are a number of new hotels expected to be developed in the next

five years, including a 150-room Marriott, a 300-room Hilton, a 250-room

Le Méridien and a number of smaller projects.

In general, Oman�s economy should continue to expand at an impressive

rate, with forecasters envisaging average real GDP growth of 5.8% in 2001

and 4.5% in 2002. The primary driver behind the spurt in growth this year

will be exports of liquefied natural gas (LNG), which are expected to double

in volume. This increase in GDP should have a positive effect on

the overall economy and on the tourism sector in particular.

Qatar

As the Qatari economy is heavily dependent on fluctuating revenues from

oil exports, the increase in oil prices during 2000 certainly helped the

government. Recognising the importance of investment for economic growth,

the Qatari government is developing an increasingly open attitude to foreign

investment. During the last two years, Qatar managed to achieve a balanced

budget despite huge debt repayments for different investments in gas refinement

projects. Forecasts indicate a significant growth in GDP for the

next few years (7.2% in 2002) as net revenues from LNG exports start to

affect the economy significantly. In fact combined revenues from oil and

LNG should result in Qatar being among the wealthiest nations, per capita,

in the world in the next few years.

Doha has seen a significant increase in visitor arrivals over the last

four years, and these are set to continue to increase in the future. In

2000, due to an increase in supply, occupancy levels in Doha decreased

by three percentage points to 58%. This decline in occupancy was only compensated

for by a small increase in average rate of 2% to US$115, one of the highest

average rates in our survey. Despite these figures, the quality hotels

in Doha are still seen to be performing relatively well.

Doha saw the addition of a 300-room Inter-Continental in October 2000.

The opening of the 369-room Ritz-Carlton planned for earlier this year

has been postponed until the fourth quarter of 2001. These two hotels are

located in the West Bay area, which is currently receiving huge investment.

In addition, there are also plans for a 376-room Four Seasons hotel, a

300-room Grand Hyatt and a 270-room Doha Rotana. These additions to supply

are expected to cause the occupancy level to dip in the coming years. The

extent of the decrease in occupancy levels will be dependent on how well

Qatar manages to market itself to a wider audience, especially considering

the current absence of a formal ministry of tourism, and on the effects

of the continuing regional conflicts.

The forecast for the next few years is positive as Qatar continues to

invest in order to attract visitors. There are plans for an extension of

the airport and also for the construction of a new retail mall. In

addition to this, Qatar will host the 2006 Asian Games. This project will

spur further investment, including a US$700 million sport city just outside

Doha.

Saudi Arabia

The government of Saudi Arabia is restructuring its economy away from

its reliance on oil exports. The windfall in oil revenue in 2000 due to

high oil prices helped to balance the budget and will allow the government

to continue with its plan to foster private sector activity. The financial

sector is healthy and the role of local banks is growing to finance private

enterprise, develop the domestic capital markets, and build financial retail

services. The key to further diversification efforts and the expansion

of Saudi Arabia�s industrial base lies in the hands of the Kingdom�s able

private sector. In addition, economic reforms and the relaxation of visa

requirements are likely to further improve the environment for foreign

direct investment.

At the time of writing, tourism figures for 2000 were not available.

However, we can report that in 1999 arrivals increased by approximately

2%. A vast majority of visitors to the Kingdom are pilgrims visiting Mecca

and Medina who, historically, were allowed to visit only these two destinations.

However, the government has recently relaxed its restrictions and visitors

may now visit other destinations in the Kingdom. This relaxation may help

visitor numbers to increase.

Occupancy levels in Jeddah increased by four percentage points to 65%;

Riyadh showed a decline of two percentage points to 60% in 2000 when compared

to 1999. Despite increases in supply, with the opening of the 284-room

Le Méridien and a 196-room Westin, average rates in Jeddah increased

by 7% to US$119 in 2000, the highest level since our survey began in 1993.

Average rates in Riyadh decreased slightly to US$115 in 2000.

Hotel supply in Jeddah is set to continue to increase over the next

few years with the opening of a 465-room Hilton (2001), a 102-room Royal

Méridien (2002), a 170-room Ritz-Carlton (2003) and the 322-room

Al Amir Tower in 2005. This large increase in supply will undoubtedly have

an adverse affect on operating performances in the future. However, continued

fiscal liberalisation and economic growth will help to increase demand

and will therefore help to absorb this supply. Additionally, the Four Seasons

development programme continues in the Middle East with a 242-room hotel

planned to open in Riyadh in 2002 as part of a large mixed-use complex.

While we are positive with respect to the economic growth of Saudi Arabia

and its capacity to implement some fiscal reforms, the strong religious

beliefs and, therefore, restrictions such as a ban on alcohol will undoubtedly

hinder any significant progress in terms of tourism growth in the Kingdom.

Nevertheless, a strong base level of demand will always be present from

pilgrims making hajj and perhaps from Gulf visitors coming to the Red Sea,

who do not want to go to the other Gulf states where there is a more liberal

attitude to tourism and alcohol is more freely available.

Syria

In March 2000, the government made a modest start in the implementation

of free market reform with the help of the new president Bashar Assad,

who is reportedly keen to move the country into the twenty-first century.

By all accounts, this reform has continued in 2001 with the early passing

of the 2001 fiscal budget and a package of financial measures intended

to stimulate an inflow of investment capital. Foreign policy issues continue

to be dominated by relations with neighbouring Israel, Syria�s support

for the Palestinian cause, and the situation in south Lebanon.

Syria is highly dependent on the international price of oil, with oil

accounting for an estimated 70% of export revenue in 2000. The forecast

decline of oil prices, combined with Syria�s unsettled political situation,

is likely to affect the country�s growth outlook. The government may come

under pressure to reconsider expenditure pledges as lower oil prices reduce

revenue, resulting in an easing of government consumption. However, growth

in private consumption, the main component of GDP, should accelerate in

2001, remaining above 2000 rates throughout the year.

Meanwhile, investment spending is likely to see some modest growth.

Although the number of visitor arrivals for the full year is not yet available,

the last estimate for 2000 was approximately 2.5 million visitors, a decrease

of 6.8% compared to 1999, largely due to the political situation in Israel.

This figure is likely to continue to decrease further as long as the situation

does not improve. Recovery after the conflict has eased should be quite

fast as Syria is fortunate in its cultural heritage and can offer a unique

product compared to other destinations in the Middle East such as Dubai

and Bahrain.

Our research indicates that operating levels in Damascus in 2000 have

decreased compared with those achieved in 1999. At 66%, the average occupancy

level has fallen by three percentage points. Average rates have also decreased,

by approximately 7%, to US$97. The result is RevPAR of around US$65, a

decrease of approximately 10% when compared to 1999.

As reported last year, the development of the 305-room Damascus Four

Seasons hotel is still planned, although this is likely to be delayed.

In addition, hotel developments are planned for other destinations in Syria,

including a 196-room Sheraton Hotel due to open in two years time in the

city of Aleppo and a further 70-room hotel and 30-chalet development in

Saydaniya.

After years of isolation, Syria is making efforts to join the free Arab

economic zone and to reach an association agreement with the European Union,

which has committed nearly US$100 million to help Syria in its reforms.

In addition some plans unveiled at the end of 2000 included legislation

to allow foreign investors to own land and set up joint ventures. The government

has promised to speed up its response time for tourism project permits.

So there are hopes of better times to come in the next few years.

United Arab Emirates

Economic diversification began at an early stage and the UAE was never

quite as dependent on oil as other Gulf states. The oil sector accounted

for around 25% of GDP in 2000, while non-crude oil goods now represent

over 50% of total exports. At the end of 2000, the overall level of economic

activity was boosted by the increase in oil prices, although domestic oil

output itself does not usually contribute strongly to growth. These higher

oil revenues, however, have filtered through the economy by increasing

government and personal expenditure and by promoting investments.

Current high oil revenues are welcomed by the UAE government but are

viewed as a windfall rather than perennial. Economic policy will therefore

continue to promote non-oil industries, private sector activity, rationalisation

of state-owned assets and a favourable, enabling business environment.

The UAE showed strong growth in visitor arrivals for 2000 of 8.1%. This

gain is understood to be largely due to the recovery of world economies

including those of Asia, the Middle East and Russia, as well as an increase

in hotel room supply and the increasing reputation of Dubai as a leisure

destination. Visitation is expected to continue to increase in the future

as hotel development continues both in Dubai and in other destinations

such as Abu Dhabi, Fujairah and Sharjah.

The rapid development of hotels in Dubai along Jumeriah Beach has had

a somewhat negative impact on hotels downtown. Dubai as a whole showed

a significant increase (4%) in occupancy levels to 74% despite the increase

in supply. Average rates decreased by around 1% in 2000 to US$105. The

growth of Dubai�s hotel supply has been well publicised as operators and

the government attempt to fill the ever-increasing number of rooms in the

city and, indeed, the country. Some of the more recent projects to open

in Dubai include the all-suite Burj al-Arab, the Emirates Tower Hotel and

the Royal Mirage, in addition to a 100-room extension at the JW Marriott

hotel downtown. The additions to supply forecast for 2001 are the 174-room

Dusit Hotel and the 156-room Hilton International. During the course of

2002, hotels planned to open include a 180-room Four Seasons hotel, a 674-room

Grand Hyatt Dubai, a 300-room Shangri-La hotel, and a 264-room Sheraton

Plaza, as well as a number of extensions to existing properties.

While this large increase in supply may suggest poor future operating

levels, the development of ancillary products and services, including a

conference centre, golf courses, water parks, shopping promotions, a cruise

ship terminal, planetarium and, possibly, a Formula 1 racetrack has enabled

and is likely to continue to enable demand to grow in the future.

We would draw particular attention to the Palm Tree Islands development

to be built off the coast of Jumeirah Beach near to the Royal Mirage Hotel.

The first of the two islands will feature 2,000 residential villas and

40 luxury boutique hotels. In addition, the islands will feature a marine

park, multiplex cinemas, health spas and a number of marinas providing

a total of approximately 600 berths and 200 �mega� yachts.

Abu Dhabi�s quality hotels saw an increase in occupancy from 64% in

1999 to approximately 67% in 2000. Average rate performance amongst the

quality hotels in 2000 showed a significant decrease of 11%, to approximately

US$88, when compared to 1999. The dampening of the economy and an increase

in supply can be said to be largely responsible for this decline. The government

has recently directed its attention to the hotel sector. This new trend

enables the Emirate of Abu Dhabi to diversify its income sources and to

enlarge the contribution of the hotel sector to the Emirate�s GDP. There

are plans to develop a luxury shopping mall and the biggest marina in the

Middle East on reclaimed land just off the corniche. In addition, there

are currently plans to develop a 292-room Marriott hotel, a 250-room Hilton

on the beachfront, a 300-room Sheraton, and to expand the Abu Dhabi Grand

(formerly the Forte Grand) hotel, which is now managed by Rotana Hotels,

by 126 rooms.

Further development is also expected to take place in Fujairah with

several projects identified as starting shortly, including one by Rotana

Hotels and a 300-room Westin hotel.

Hotel Development

Last year we reported that many of the countries featured in our survey

felt that tourism was an important source of revenue for the future in

light of the decreasing oil revenues in 1999. Many of the countries reported

rapid changes to promote investment in

| tourism; however, financially and

structurally, they were not in a position to implement these changes. The

improved oil prices have now enabled countries to increase their tourism

budgets and many of the countries in our survey are now |

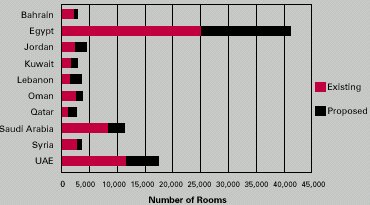

Table 10: Room Supply by Country

Source: HVS International |

trying to follow Egypt and the UAE, which, lead the region in terms of

hotel development. In addition to real progress towards achieving peace

in the region, it will take time and dynamism for these countries to produce

an attractive tourism product. HVS International has identified some 140

major first class hotel developments, which would add a further 38,000

rooms over the next four to five years if they all go ahead. In addition,

there are many more developments in the region that are at this stage within

the mid-market category and/or independently operated.

Egypt continues to be keen to expand its hotel supply throughout the

country; however, development is still concentrated along the Red Sea coastline

which is in danger of becoming similar to the Spanish Costa del Sol in

years to come. Visitor arrivals were again at record levels in 2000, and

by all accounts the supply-led demand is proving to be successful for the

country. Nevertheless, the continued lack of improvement in terms of infrastructure

in Egypt is likely to have some negative repercussions in the future. In

particular there has been a severe lack of investment in Egypt�s air infrastructure,

specifically in terms of improving and expanding airport capacity. In addition,

there is still a lack of scheduled flights, which will severely limit the

Red Sea resort areas and their ability to promote themselves to conference

and incentive demand (especially in the low season) and to higher-end leisure

demand.

On the other hand, the expansion of Dubai as a destination continues

unabated, and plans are underway to dramatically increase the area�s hotel

supply further in the coming years. However, this increase in supply

is coupled with ancillary developments, as opposed to stand-alone hotel

developments, as are typical in Red Sea destinations such as Sharm el Sheikh

and Hurghada.

The lack of real progress in the peace process has had some negative

impact on tourist arrivals in the region. However, Dubai and countries

such as Egypt have successfully marketed themselves as being somewhat removed

from the day-to-day tension and sporadic conflicts between Israel and the

Palestine Authority.

Hotel development does not seem to have slowed down since our report

last year and hotel management companies are confident that the region

will achieve substantial growth over the medium to long term. Although

this rapid development in the region is encouraging, close attention will

have to be paid to such issues as infrastructure development, human resource

training and relaxation of visa controls, including multiple country visas,

to encourage cross-border tourism. The countries that pay attention to

these issues will ultimately benefit most in the future.

Hotel Development by Chain

Typically, the major brands such as Bass (6 Continents), Starwood, Le

Méridien and Marriott continue to show the most aggressive expansion

plans in the Middle East and most are looking to achieve multiple brands

in some cities; Dubai, for instance, has a Ritz-Carlton, JW Marriott and

Renaissance. Reports have suggested that competition for management contracts

amongst hoteliers is extremely strong thereby ensuring that management

fees are slowly but surely decreasing and that contract terms are becoming

less favourable to operators as owners search for the best deal.

The emergence of high-quality brands such as Ritz-Carlton, Four Seasons

and Kempinski will hopefully help in attracting high-end European, Asian

and American travellers to the region not only for business but, equally

importantly, for conference, incentive, and leisure trips. However, the

continued regional tensions, together with difficulty in obtaining multi-destination

visas and poor infrastructures, will hinder some of this progress in the

future.

Rotana Hotels, a regional brand, is continuing to increase its reputation

throughout the Middle East and has recently introduced a loyalty programme.

It also has plans to expand into new countries such as Syria and Egypt.

Conclusion

The economies of most countries in the Middle East region improved in

2000, and economic predictions for the next few years are generally positive

for the most part. Most of the countries featured in this survey have pledged

to increase foreign direct investment and privatisation, improve fiscal

policy and to encourage diversification of their revenue sources.

However, many Middle Eastern governments are still slow to allow economic

reform and encourage privatisation and foreign investment. This stifling

of economic progress is in turn restricting investment in infrastructure

such as airports, where capacity has in some cases already been reached

and is no longer sufficient to accommodate the demand for hotels in the

area.

Other issues that will need to be addressed in the future include the

development of ancillary services such as marinas, golf courses, retail

outlets and leisure parks, such as is currently taking place in Dubai.

Furthermore, the relaxation of visa restrictions to allow visitors to move

more freely between countries, and training of and investment in local

human resources, will greatly enhance the region�s ability to realise its

full potential.

Operating performances for hotels in the region were generally much

improved in 2000 compared to 1999, largely assisted by the improvement

in oil prices and the relatively stable peace process. RevPAR for the region

was at one of its highest levels for seven years with both occupancy and

average rate increasing. Demand in the region is expected to continue to

increase; however, increasing supply levels are likely to have a detrimental

impact on operating levels in some destinations. The Middle East,

in general, has realised that tourism is likely to become an increasingly

important source of national revenues in the next few years. Many

countries have followed the lead of Egypt and, more importantly, Dubai

in encouraging investment into this sector. Unfortunately, although this

investment has been taking place in some countries, it often lacks the

commitment and national backing that it has enjoyed in Dubai. Nevertheless,

it is likely that demand for hotels throughout the region will continue

to increase significantly in the future.

--

Gerard Greene is a Senior Associate with HVS International�s London Office.

Gerard has operational experience with both Marriott and Hyatt in the USA.

Since joining HVS in late 1997, Gerard has worked on numerous assignments

throughout the Middle East, Europe, Africa and Asia.

HVS International is also grateful for the assistance of Yannick Simonart

in the research and preparation of this report.

© 2001 HVS International. All rights reserved. |